Iron Bear Resources Limited (ASX: IBR) — Indicated Resource Doubles to 4.5 Billion Tonnes at 29.5% Fe and 20.6% Magnetic Fe at the Iron Bear Project

- Noel Ong

- May 18

- 18 min read

Australian-Domiciled Iron Ore Developer Advancing the Iron Bear Magnetite Project in the Labrador Trough, Canada

ASX: IBR | Iron Ore Development | Labrador Trough, Canada |

|---|

Iron Bear Resources Ltd (ASX: IBR) is advancing a magnetite iron ore project in a jurisdiction that has been producing iron ore since 1954, and that hosts some of the world's most established direct-reduction-grade producers.

Our fascination as a shareholder with the Iron Bear story can be measured by three attributes that matter most for a development-stage magnetite story. The first is scale that is genuinely global, the second, metallurgical results that demonstrate a Direct Reduction-grade concentrate is achievable at industrial pilot scale, and finally, one of the most important parts, infrastructure proximity that is not theoretical but operational.

The Iron Bear project sits within 35km of an open-access heavy-haul railway connected to the Sept-Îles and Pointe-Noire iron ore export ports, with access to low-cost renewable hydroelectric power.

The 13.6 billion tonne Mineral Resource which 4.5 billion tonnes is now Indicated , technically places the project among the largest magnetite endowments held by an ASX-listed developer.

The 71.0% Fe and 1.2% SiO₂ DR-grade pilot concentrate result is a number that puts Iron Bear's potential product specification within the upper band of what the global decarbonisation steel transition is calling for.

Indicated Mineral Resource Lifts 114% to 4.5Bt at 29.5% Fe, Strengthening the Foundation for the Iron Bear Project in the Labrador Trough

Samso Insights | ASX: IBR | Source: Iron Bear Resources Limited ASX Release, 12 May 2026

Introduction

Iron Bear Resources Limited has released its 2026 Mineral Resource Estimate Update for the Iron Bear Iron Ore Project in the Labrador Trough region of Newfoundland and Labrador, Canada (Figure 1).

Figure 1: Iron Bear - Regional Access and Infrastructure. (source: Iron Bear Resources Limited)

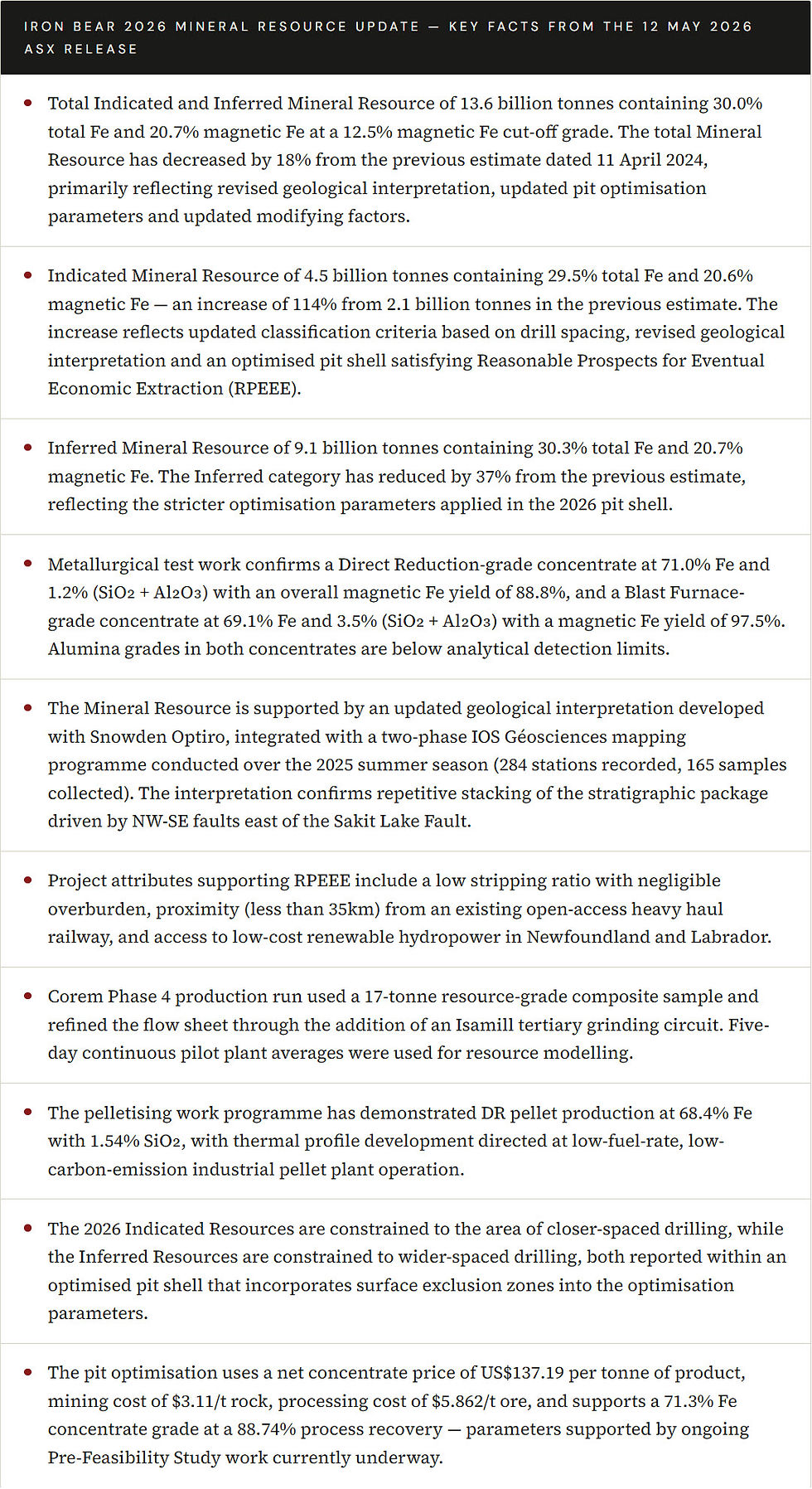

The headline number from the announcement is the 114% increase in the Indicated category, from 2.1 billion tonnes in the previous April 2024 estimate to 4.5 billion tonnes in the current estimate, at a grade of 29.5% total Fe and 20.6% magnetic Fe.

The total Indicated and Inferred Mineral Resource sits at 13.6 billion tonnes containing 30.0% total Fe and 20.7% magnetic Fe, reported at a 12.5% magnetic Fe cut-off grade.

The total resource has decreased by 18% from the previous estimate, which the company attributes to revised geological interpretation, updated pit optimisation parameters, and application of updated modifying factors.

Readers should see the significance of this update in the potential methodology shift behind it.

The 2024 Indicated category was defined by reference to a "30-year pit shell". The 2026 Indicated category is defined by reference to closer-spaced drilling supported by an optimised pit shell that satisfies Reasonable Prospects for Eventual Economic Extraction (RPEEE) requirements.

The reduction in the total resource is therefore not a reflection of less mineralisation — it is a reflection of a stricter application of constraints. The trade-off is a much larger Indicated category, which is the category that can support more advanced technical studies and is the foundation from which Ore Reserves are ultimately derived. For a development-stage company, this is a meaningful methodological maturation.

The Mineral Resource update is supported by an updated geological interpretation developed in conjunction with Snowden Optiro, integrated with field mapping completed by IOS Géosciences across 284 stations during the 2025 summer season, and underpinned by four phases of pilot-plant scale metallurgical test work at Corem in Canada.

The metallurgical work confirms that the Iron Bear deposit can produce a Direct Reduction-grade concentrate of 71.0% Fe and 1.2% SiO₂ at an overall magnetic Fe yield of 88.8%, and a Blast Furnace-grade concentrate of 69.1% Fe and 3.5% SiO₂ at a magnetic Fe yield of 97.5%.

These are pilot-plant production-run averages, not single-day peaks, and are the basis on which the resource has been optimised for RPEEE.

Highlights

2026 Mineral Resource Estimate Detail

Iron Bear Mineral Resource Estimate at 12.5% Magnetic Fe Cut-Off (Effective Date 5 May 2026)

Table 1: The Mineral Resource Estimate. (source: Iron Bear Resources Limited ASX Release, 12 May 2026 (Table 2). Inferred Mineral Resources have a lower level of geological confidence and must not be converted to Ore Reserves and do not have sufficient confidence to support economic studies.)

Global Peer Comparison

How Iron Bear's Magnetite Grades Compare to Major Global Magnetite Operations and Developments

Magnetite iron ore deposits are not assessed in the same way as direct-shipping hematite ores. The head grade and the in-ground iron percentage is typically lower than for hematite deposits, because magnetite ores are designed to be processed through grinding and magnetic separation into a high-grade concentrate.

What matters in a magnetite assessment is the combination of three things: the in-ground magnetic Fe percentage (which drives recovery and tonnes-to-concentrate ratio), the concentrate Fe specification achievable from metallurgical work, and the impurity profile (particularly SiO₂ and Al₂O₃) of the final concentrate.

The table below benchmarks Iron Bear against a selection of major global magnetite operations and developments on those parameters.

Table 2: Global magnetite deposit comparisons. (sources: Public company disclosures, JORC/NI 43-101 reports, Geoscience Australia Australian Resource Reviews, S&P Global Commodity Insights, and operator websites accessed May 2026. Concentrate specifications refer to production-run or pilot-plant averages; in-situ head grades refer to current Mineral Resource or Reserve grades at stated cut-offs. Iron Bear concentrate specifications are pilot-plant production-run averages (Corem Phase 4).)

The relevant observation from this comparison is not the in-ground head grade which for a magnetite BIF is always going to fall in a range that reflects the geological character of the host rock.

The Iron Bear in-ground grade of 29.5% Fe / 20.6% magnetic Fe sits within the typical range for Lake Superior-type taconite operations globally, comparable to Sino Iron at ~28-30% Fe and the Mesabi Range taconite operations at ~25-30% Fe.

What separates Iron Bear from the lower-grade end of this peer group is the concentrate specification. A 71.0% Fe DR-grade concentrate at 1.2% SiO₂, with alumina below analytical detection limits, is at the upper specification band of the global magnetite industry. It is comparable to what Bloom Lake (Champion Iron) is targeting from its DR-grade pellet feed upgrade project at 69% Fe, and approaches the LKAB Kiruna premium pellet feed specifications.

Readers should remember that the concentrate purity is a function of both the favourable mineralogy at Iron Bear (low alumina, low phosphorus, low manganese) and the flow sheet's inclusion of reverse flotation and tertiary grinding to break apart any composite magnetite-quartz particles.

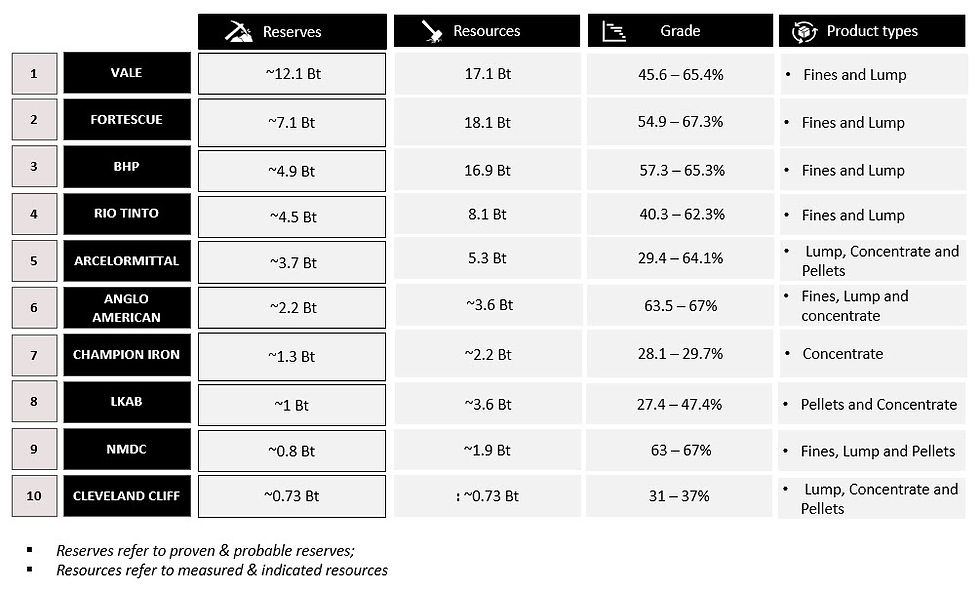

Table 3: Top 10 Global Iron Ore Producers by Proven & Probable Reserves. Note that the top 4 alone account for over 80% of reserves among the top 10, which is a concentration that defines long-term supply dynamics. (Source: Vale, BHP, Wikipedia, Rio Tinto, Champion Iron, Cleveland Cliff, LKAB, ArcelorMittal Anglo America)

What is very interesting is that the global concentration of iron ore producers as shown in Table 3 show that the top 4 producers in a list of a global top 10 list of producers, account for over 80% of reserves. This is very important when you take into context that Iron Bear Resources Limited has Vale as a funding partner.

For the shareholders of Iron Bear Resources, this is very important as the upcoming release of the PFS is going to need a Tier-1 partner to fund the Iron Bear project. The Iron Bear project is not a small project, it is in the scale of all the major iron projects. This is a very important fact to remember because investors could be blindsided by the very low market capitalisation of Iron Bear Resources Limited.

Last 5 Major Iron Ore Projects Developed (to May 2026)

Ranked by scale of investment and significance, with all figures cross-checked against company disclosures and recent reporting up to early 2026:

1. Simandou — Guinea

Operators: Rio Tinto SimFer (Blocks 3 & 4) and Winning Consortium Simandou / Baowu (Blocks 1 & 2)

Ownership of SimFer: Rio Tinto 53%, Chalco Iron Ore Holdings 47% (with Guinea Government holding 15% in the mining concession company)

CAPEX: Total project investment of approximately US$20 billion (Wikipedia/industry summary including rail and port). The Simfer joint venture alone has a capital funding requirement of approximately US$11.6 billion, of which Rio Tinto's share is approximately US$6.2 billion.

Status: First shipment left Guinea in December 2025. Ramping up over 30 months to 60 Mtpa from the SimFer mine, with combined Simandou (SimFer + WCS) capacity up to 120 Mtpa.

Grade: ~65% Fe high-grade hematite — described as the world's largest untapped high-grade iron ore deposit.

2. Onslow Iron — Pilbara, Western Australia

Operator: Mineral Resources Limited (MinRes, ASX: MIN) on behalf of the Red Hill Iron Joint Venture

JV Partners: MinRes (60.3%), China Baowu Steel Group, AMCI, POSCO

CAPEX: Approximately A$3 billion (~US$2 billion). MinRes subsequently sold a 49% interest in the dedicated haul road to Morgan Stanley Infrastructure Partners for total expected proceeds of A$1.3 billion.

Status: First ore on ship May 2024, ahead of schedule. Reached nameplate capacity of 35 Mtpa in 2025. Expected mine life of more than 30 years.

Grade: Hematite Direct Shipping Ore

3. Iron Bridge — Pilbara, Western Australia

Operator: Fortescue (FMG Magnetite Pty Ltd)

JV Partners: FMG Magnetite (69%, owned by Fortescue and Baosteel) and Formosa Steel IB (31%)

CAPEX: US$3.9 billion total (Fortescue share approximately US$3.0 billion). The project blew out from an original estimate of US$2.6 billion at FID in 2019.

Status: First magnetite production May 2023. Ramp-up has been slower than planned — revised guidance now sees nameplate of 22 Mtpa not reached until FY2028 (a full five-year ramp from first production).

Grade: 67%+ Fe high-grade magnetite concentrate

4. Western Range — Pilbara, Western Australia

Operator: Rio Tinto

JV Partners: Rio Tinto (54%), China Baowu Steel Group (46%)

CAPEX: US$2 billion (Rio Tinto share US$1.3 billion). Completed on time and on budget.

Status: First ore processed late March 2025. Officially opened June 2025. Capacity of up to 25 Mtpa, sustaining the Paraburdoo mining hub for up to 20 years.

Grade: Pilbara Blend hematite

5. Serra Sul +20 Mtpy (S11D Expansion) — Carajás, Brazil

Operator: Vale S.A.

CAPEX: Approximately US$2.8 billion

Status: Operating licence received from IBAMA in September 2025; commissioning scheduled for the second half of 2026. As of July 2025 the project was at 77% physical progress and 57% financial progress.

Capacity Add: Lifts S11D mine-plant capacity by 20 Mtpa to approximately 120 Mtpa.

Grade: ~65% Fe Carajás high-grade fines

Total Capital Deployed Across These Five Projects

Approximately US$30 billion in headline project investment (using the lower Simfer-only figure of US$11.6 bn for Simandou rather than the total US$20 bn integrated figure).

Thoughts To Ponder

The CAPEX figures highlight just how capital-intensive new iron ore development has become. The smallest of these — Western Range at US$2 bn — is a sustaining brownfield project that leveraged existing Paraburdoo infrastructure.

Simandou, the largest, required US$20 billion in part because it had to build 622 km of greenfield railway and a deep-water port from scratch. Infrastructure is the variable that swings project cost most heavily.

The two magnetite projects on the list (Iron Bridge and the still-developing context of what Iron Bear faces) tell their own story. Iron Bridge ran from US$2.6 bn to US$3.9 bn through construction and is now in a multi-year slow ramp.

That's the lesson that's most relevant to the Iron Bear context. This is why the infrastructure proximity of the Labrador Trough (existing rail, existing ports, existing hydro) is genuinely material to any project economics in that region versus building greenfield in the Pilbara.

The Kami Project, which I referenced in a previous Samso Insight (see below) as a development-stage Labrador Trough peer, is currently estimated at approximately US$4 billion to bring into production is the most useful as a benchmark for what an undeveloped DR-grade magnetite project of similar scale might require.

The Australian Magnetite Scene

The Australian magnetite industry has been described in industry commentary as having a "checkered past" — Sino Iron and Karara are well-documented examples of major cost overruns, slow ramp-ups and challenging economics. The lesson from those operations is that low head grade combined with high beneficiation cost can produce a project that struggles to compete with hematite Direct Shipping Ore producers.

What makes A Magnetite Project Work

The variable that determines whether a magnetite project is commercially viable is whether the concentrate it produces commands sufficient premium to offset the additional processing cost. That premium is being increasingly driven by demand for DR-grade pellet feed (above 67% Fe, with low silica and alumina) from electric arc furnace (EAF) and hydrogen-based direct reduction iron (DRI) steelmaking — the routes that are central to the global steel industry's decarbonisation pathway. Iron Bear's pilot-plant concentrate specifications place it within the DR-grade window that this consistent to this market segment.

Regional Peer Comparison

Iron Bear in the Context of Labrador Trough and North American Magnetite Peers

The Labrador Trough is one of the most established iron ore regions in the world, with continuous production dating to 1954. The region currently produces approximately 50 million tonnes per annum across producers including Rio Tinto's Iron Ore Company of Canada (IOC) operation at Labrador City, ArcelorMittal's Mont-Wright operation in Quebec, Champion Iron's Bloom Lake mine, and other regional producers (Table4).

The Iron Bear project sits within the same geological belt , the Sokoman Formation, that hosts these operations, but with its own particular structural characteristic: the deposit has been thickened by repeated thrust faulting that has stacked the mineralised stratigraphy across more than 500 vertical metres of section. The table below benchmarks Iron Bear against its Labrador Trough and adjacent North American magnetite peers.

Table 4: An attempt to create a Labrador Trough peer comparison. (sources: Champion Iron corporate filings, Rio Tinto Labrador Iron Ore (LIORC) disclosures, Champion Iron / Nippon Steel / Sojitz Kami Project partnership announcements, ArcelorMittal Mining Canada disclosures, and Cleveland-Cliffs operational reports. Comparison is for illustrative context only and does not represent equivalent reporting standards across all entries.)

The Labrador Trough peer comparison clarifies what Iron Bear is and what it is not. Iron Bear is not yet a producer. Bloom Lake, IOC, and Mont-Wright are all operating mines that have been shipping concentrate for decades or in Bloom Lake's case, they have completed a major Phase II expansion and are now investing in a DR-grade upgrade.

The peer that most resembles Iron Bear's current stage of development is the Kami Project, which is also a development-stage DR-grade-targeted project, also in the Labrador Trough, also without a final investment decision.

Kami's announced partnership with Nippon Steel and Sojitz provides a useful benchmark for the scale of investment that DR-grade Labrador Trough development represents, which is that the Kami partners have indicated up to US$490 million of partner funding ahead of Champion's pro-rata contribution, and the project has been described as requiring an investment in the order of US$4 billion to bring into production.

What Iron Bear does have in common with the Labrador Trough producers, and what is distinct from the Australian magnetite peer group, is the geological character of the mineralisation.

The deposit is a Lake Superior-type banded iron formation hosted in the Sokoman Formation — the same stratigraphic unit that hosts Bloom Lake, IOC's Carol Lake, and the historical Schefferville direct-shipping ores.

The 2025 mapping conducted by IOS Géosciences confirmed three main NW-SE repetitions of the stratigraphic package in the southeastern portion of the property, identifying previously unrecognised iron formation between Boot Lake and Burnetta Lake and north of Nash Lake.

The 2026 geological interpretation incorporates the structural complexity that is characteristic of the eastern Labrador Trough, where thrust faulting has repeatedly stacked the iron formation. This is the same geological process that has produced the multi-billion-tonne deposits underpinning Bloom Lake, Mont-Wright, and IOC.

The comparison that matters here is geological provenance. Iron Bear's host rock is the same as the host rock for the established producers; its DR-grade concentrate specification falls within the same band as the regional producers; and its proposed processing flowsheet uses techniques that are well-established in Labrador Trough operations.

Figure 2: Iron Bear - Regional Geology and Historic Drilling. (source: Iron Bear Resources Limited)

Metallurgical Test Work — Pilot Plant Production

Pilot Plant Concentrate Production: Corem Phase 4 Confirms the DR-Grade Product Specification

The 2026 Mineral Resource estimate is supported by four phases of metallurgical test work conducted at Corem in Canada, culminating in Corem Phase 4 — a 17-tonne resource-grade composite that produced bulk customer samples and informed the pellet plant thermal profile design. The Phase 4 production-run results have been used as the basis for the resource modelling factors and pre-feasibility study design factors. The table below summarises the production-run concentrate chemistry across the four phases:

Table 4: Metallurgical Test Work - Pilot Plant Production. (source: Iron Bear Resources Limited ASX Release, 12 May 2026 (Tables 8 and 9). Phase 4 results were obtained as five-day continuous pilot plant averages and are used as the basis for resource modelling and PFS design factors. Alumina (Al₂O₃) grades in both BF and DR concentrates are below analytical detection limits.)

The progression from Phase 1 to Phase 4 demonstrates that the concentrate specifications are reproducible across different feed grades and that the addition of column flotation in Phase 4 — replacing conventional reverse flotation — has materially lifted DR concentrate magnetic Fe recovery from 80.7% in Phase 1 to 88.8% in Phase 4. The presence of an Isamill as a tertiary grinding circuit, introduced in Phase 4, was specifically added to break apart any larger composite particles of magnetite and quartz observed in the +45 micron size fraction. The technical implication is that the flowsheet is converging on a configuration that delivers a consistent DR-grade product at high recovery — which is the technical foundation on which a magnetite project's commercial case is built.

Management Commentary

What the Company's Leadership Said About the Mineral Resource Update

Paul Berend, Managing Director and CEO of Iron Bear Resources, characterised the updated Mineral Resource as an important and exciting milestone for the project. His commentary focused on the significance of the Indicated Resource increase and on what it represents for the foundation of the company's ongoing technical studies. The Pre-Feasibility Study is being led by global engineering firm Hatch, and the resource update is the technical input that feeds the optimised mine plan associated with that study.

"This Mineral Resource Update is an important and exciting milestone for the Iron Bear project. We now have an indicated mineral resource of 4.5 billion tonnes which strengthens the foundation for ongoing technical studies."

— Paul Berend, Managing Director and CEO, Iron Bear Resources Limited

The technical detail of the resource update is supported by the work of independent consultants. The Mineral Resource Estimate has been prepared by Mr Michael Andrew FAusIMM, a full-time employee of Snowden Optiro, who is the Competent Person responsible for the estimate.

The metallurgy and processing information has been reviewed and compiled by Mr Paul Vermeulen MAusIMM, MAIST, a Director of Vulcan Technologies Pty Ltd. Both consultants have provided sign-off in accordance with the JORC Code (2012) reporting standards.

Near-Term Milestones to Watch

What Investors Should Monitor Following the 2026 Mineral Resource Update

Samso Concluding Comments

Putting the Iron Bear Mineral Resource Update in Context

Investors and potential investors should look at the 12 May 2026 ASX release from Iron Bear Resources as a meaningful technical step. What this meaningful step is the 114% increase in Indicated Resource.

The 2024 Mineral Resource defined the Indicated category by reference to a "30-year pit shell". The 2026 Mineral Resource defines the Indicated category by reference to drill spacing, supported by an optimised pit shell that incorporates RPEEE constraints and surface exclusion zones.

This is a stricter approach. It is also the approach that is more typically applied at the pre-feasibility stage of project development. The Indicated category has doubled under a stricter methodology rather than shrinking, which in most cases is the opposite. It reflects the closer-spaced drilling at the heart of the resource, supported by the structural reinterpretation that came out of the IOS Géosciences mapping work and the Snowden Optiro modelling (Figure 3).

Figure 3: Preliminary Geological Map (LHS) vs Model (Middle) vs Geophysics comparison (RHS) at Iron Bear

The peer comparison context is what gives the resource update its commercial dimension. A 4.5 billion tonne Indicated Resource is simply a very large resource, regardless of where it sits. But the value of that resource is determined by what can be produced from it, and the Corem Phase 4 metallurgical work has provided the answer that matters most: a 71.0% Fe DR-grade concentrate at 1.2% SiO₂ with alumina below detection limits, at 88.8% magnetic Fe recovery, produced from a 17-tonne pilot-plant production run.

That concentrate specification places Iron Bear within the upper specification band of the global magnetite industry, alongside Bloom Lake's planned 69% Fe DR-grade upgrade, the LKAB Kiruna pellet feed product, and the Kami Project's targeted 67.5%+ Fe DR-grade specification.

The difference between a 65% Fe blast furnace product and a 71% Fe DR-grade product is not marginal in commercial terms — it is the difference between selling into the conventional integrated mill market and selling into the decarbonisation steel market where premium pricing is established and growing (See the Samso Insight below).

Figure 4: Examples of DR Pellets.

The infrastructure context is the third leg of the assessment. Magnetite projects globally have struggled, where the infrastructure case has been built on assumptions rather than operational reality.

Karara and Sino Iron in Western Australia both had to build new rail, port and water infrastructure to support magnetite production. In terms of accounting, these are capital line items that materially affected the cost of those projects.

The Iron Bear project sits within 35km of an existing open-access heavy haul railway that is currently being used by Rio Tinto's IOC, ArcelorMittal, Champion Iron, Tata Steel and Tacora to ship approximately 50 million tonnes per annum of iron ore concentrate to the Sept-Îles and Pointe-Noire ports. The rail line is operating. The ports are operating. The power is available from Newfoundland and Labrador's hydroelectric grid which is the same Churchill Falls hydroelectric system that has historically underpinned the regional industrial base. This is the operational infrastructure case that Australian magnetite projects have generally lacked.

Iron Bear is a development-stage company that has market capitalisation of AUD $62M (as of 14th May 2026). The Pre-Feasibility Study is still in progress and should be primed to be release soon. How many companies at this stage is valued at this range?

For investors watching this story, the question is no longer whether the Iron Bear project has a meaningful resource. The 12 May 2026 announcement answers that question. The question is what the published PFS will say about the capital intensity of bringing such a resource into production, what the proposed production rate will be, what the strip ratio and operating cost profile look like in study-level detail, and what the financing pathway is for what will inevitably be a multi-billion-dollar development.

The Labrador Trough peer set has demonstrated that DR-grade magnetite projects of this scale can attract major partners and that is pretty much answered with Champion Iron's Kami Project partnership with Nippon Steel and Sojitz. Iron Bear has Vale as a paying partner now.

Previous Samso News Coverage

Samso has followed Iron Bear Resources (formerly Cyclone Metals) across multiple ASX releases. The following represents our prior published coverage of the company:

April 12, 2026

January 5, 2026

September 3, 2025

August 13, 2025

July 31, 2025

March 24, 2025

March 9, 2025

About Iron Bear Resources Limited (ASX: IBR)

Australian-Domiciled Iron Ore Developer Advancing the Iron Bear Magnetite Project in the Labrador Trough, Canada

Iron Bear Resources Limited (formerly Cyclone Metals Limited, renamed in January 2026) is an Australian-domiciled mineral development and investment company focused on advancing the Iron Bear magnetite iron ore project located in the Labrador Trough region of Newfoundland and Labrador, Canada.

The project consists of ten licences totalling 7,275 hectares on 291 graticular Mineral Claims, situated approximately 30 km northwest of Schefferville, Quebec, and 1,200 km northeast of Montréal. The mineralisation is a Lake Superior-type banded iron formation of the Sokoman Formation — the same host stratigraphy that has underpinned operating mines in the region for seven decades.

The company's strategy is to develop a long-life magnetite operation producing Direct Reduction (DR) and Blast Furnace (BF) grade iron ore concentrates, supported by a 1.6t to 17t pilot plant metallurgical test work programme conducted at Corem in Canada.

The Iron Bear project lies within 35 km of an existing open-access heavy haul railway connected to the Sept-Îles and Pointe-Noire iron ore export ports, and benefits from access to low-cost renewable hydroelectric power. The company has received development funding support from Vale.

ASX: IBR Iron Bear Resources Limited | 2026 Mineral Resource Estimate Update — Iron Bear Project, Labrador Trough, Canada | ASX Release 12 May 2026

The Samso Way – Seek the Research

Here at Samso, we pride ourselves on delivering content for investors that is independent and informed by over three decades of experience in the industry. Our content is well-researched and is only created if I see merit in discussing the company's story.

Our mission is simple: cut through the noise and spotlight what matters—genuine stories, grounded insights, and real opportunity.

Our content is well-researched and is only created if the team sees merit in discussing the company or concept. Investors can explore our three core platforms:

There may be numerous paths to success in investing, but the common thread among successful individuals is that they remain committed to making informed decisions. Equip yourself with the right knowledge and tools, and you will be well on your way to achieving your financial goals.

Most importantly, investors need to be absolutely diligent in understanding their own risk-reward tolerance and capabilities. Never bite off more than you can chew. As they say, Rome wasn’t built in a day, and the Great Wall stood because it took centuries to complete.

The Samso Philosophy:

Stay curious. Stay sharp. And remember—digging deeper always uncovers the real value.

In Life, there is no such thing as a Free Lunch.

Never bite off more than you can chew is my parting comment.

Happy Investing, and the only four-letter word you need to know is DYOR.

To support our independent nature of our work, please head over to our Support Page and give us a helping hand in any of the ways listed. This is a new initiate for the Samso Platform, and it was always the concept of Samso when we started this journey in 2018.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints.

Share to Grow: Your Bonus

Samso has just released an eBook: How to Add Value to your Share Portfolio

|A lesson on geological models sought by mining companies that gives insight and an understanding of which portfolios are better - and potentially more lucrative – investments. Click here to download this eBook.|

If you find this article informative and useful, please help me share the information. I try to write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters. If you or your organisation sees the benefit of what Samso is trying to achieve and has a need to share your journey, please contact me at noel.ong@samso.com.au.

Samso is a trusted platform that equips dedicated investors with up-to-date industry knowledge and insigh0ts from top CEOs and thought leaders. By staying informed on business advancements and market trends, investors can enhance their financial decisions through a combination of expert guidance and their own research.

Samso Insights | www.samso.com.au | An Investor Lens on ASX-Listed Companies

Comments