The overselling of Encounter Resources— a niobium number two priced like an afterthought

- Noel Ong

- 3 minutes ago

- 15 min read

As the ASX small-cap market is showing a slowness in hype, is Encounter Resources simply a case the market may be missing the potential value to come.

Encounter Resources sits on a globally significant niobium resource next door to the most celebrated discovery on the ASX critical-minerals board, the WA1 Resources Limited (ASX: WA10, Luni Niobium Project. . Yet it trades at a fraction of its neighbour's value, and the gap has widened even as the resource has grown. This Insight asks a simple question: is that discount a fair read of a lower-grade, less-advanced asset — or is the market overselling a story that is about to add the one thing it is missing, confidence?

Samso News | Sector & Commodity Pillar | Critical Story - Niobium | Sector & Commodity Pillar |

1.00 — THE FRAME

A discount that grew while the asset did - The Encounter Resources Issue

There is a particular kind of mispricing that small-cap resource investors learn to watch for: the moment when a company keeps delivering good news and the share price keeps drifting the other way. Encounter Resources (ASX: ENR) has spent the past year growing its niobium resource by more than half, posting strong metallurgy, lodging a mining lease, and signing a battery partnership, while its shares fell from a 52-week high near $0.62 to about $0.255 by mid-June 2026 (Figure 1).1,2

If you take the longer term view of the share price since early 2023, which was the start of the strings of discoveries, ENR has only just doubled its value and pretty much wiped out all the gains since that time (Figure 1).

Figure 1: The share price chart for Encounter Resources Limtied as of 2nd July 2026. (Source: Commsec).

As investors reading this Samso Insight, the discussion that is being highlighted is whether this fall in valuation is something that opportunistic investors should take note. The obvious sight now is that when the operational news and the share price point in opposite directions for long enough, one of two things is true: either the market knows something the announcements don't, or the announcements contain something the market hasn't yet priced.

Lets lay out both readings from Encounter's own public record, and try and identify the single event most likely to settle the argument.

What this note is — and isn't This is a research and education piece in Samso's Sector & Commodity pillar. Every project figure below is sourced to an Encounter ASX release or a named third party. It is deliberately a two-sided read: the bull case is stated plainly because it is under-discussed, and the bear case is given its own section rather than buried. It is not a recommendation. Do your own work. |

2.00 — WHY NIOBIUM, AND WHY IT'S WATCHED

A small market with an outsized strategic problem

Niobium is a quiet metal with a supply story into the steel, a micro-alloy that makes structural steel lighter and stronger which is a smaller, faster-growing tail of high-tech uses across superconductors, aerospace, medical imaging and, increasingly, batteries.3

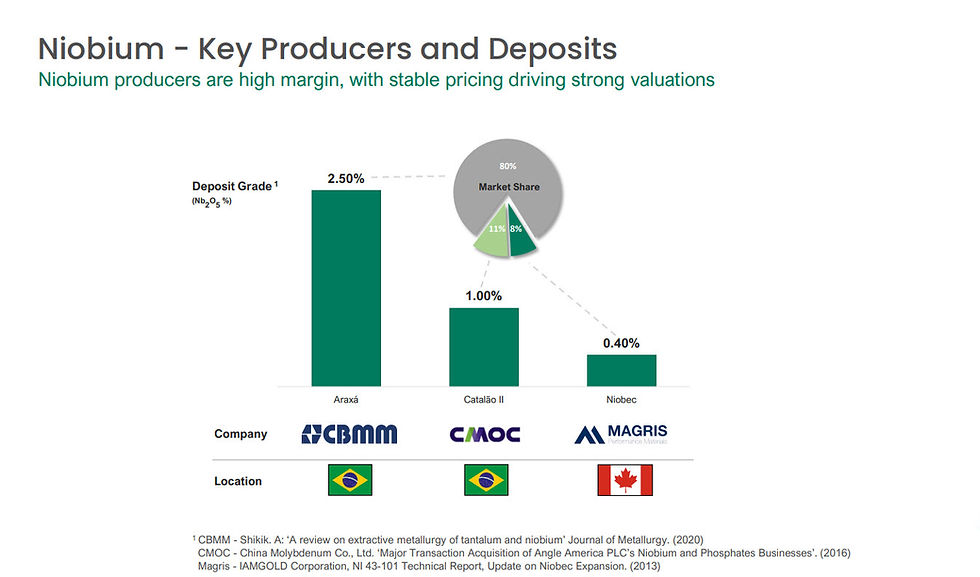

The reason it sits high on critical-minerals lists is concentration, not scale. The entire global market is only around US$5 billion, yet supply comes from essentially three mines (Figure 1.1) two in Brazil, where CBMM is the dominant producer, and one in Canada.3,4 Ferroniobium fetches roughly US$30,000/t and niobium oxide about US$45,000/t.3

A market that small, supplied by that few, is exactly the kind of supply chain that governments now want diversified — which is why a new, high-grade source in a Tier-1 jurisdiction like Western Australia attracts attention out of proportion to the tonnes involved.

Figure 1.1: The western niobium supply base is tiny and high-margin: three producers (two in Brazil, one in Canada) anchor a ~US$5 bn market, which is why a new high-grade source draws attention out of proportion to its tonnes. (Source: ENR investor presentation, 2 Mar 2026).

There is also an optionality layer the market has started to notice. Niobium-anode battery technology which is led by Cambridge-based Echion Technologies, backed by CBMM has been moving from the lab toward commercial deployment, with applications in fast-charging, long-life cells and grid-scale storage.5 On 27 May 2026 Encounter signed an MoU with Echion and Perth-based Switch Technologies to work toward an integrated lithium-niobium battery industry in Australia anchored on Aileron.5 That is not a revenue line; it is a signal about where downstream demand could go, and it sits as free upside on top of the resource story.

Samso take Niobium's investment case is the inverse of most commodities: the prize isn't a giant market, it's a strategically fragile one. For an explorer, that means the bar to relevance is "can you be a credible non-Chinese-aligned, non-Brazilian source of high-grade material" and on grade, Encounter is trying to make its case. The battery angle is the call option, not the thesis. |

3.00 — THE NEIGHBOURHOOD

West Arunta, and the shadow of Luni

To understand Encounter's valuation you have to understand WA1 Resources. In a remote corner of east-central WA, WA1 made the Luni niobium discovery in November 2022. WA1 made a find of global significance that turned a roughly $7 million company at IPO into one carrying a market cap above A$1 billion.4

Luni rewrote what the market thought the West Arunta was for both WA1 and Encounter (Figure 2)had originally gone there hunting iron-oxide copper-gold and orogenic gold, and found niobium instead.4

Luni is the benchmark every other West Arunta niobium project is now measured against: a mineral resource of 220 Mt at 1.0% Nb₂O₅ in the Indicated category, with higher-grade subsets capable of becoming starter pits, and a company already in mine-design and study stage.4

I feel that one of the main issue for Encounter is that the asset is "the other one" and being the other one to a market darling may be Encounter's biggest tailwind (it validated the province) and its heaviest weight (it framed ENR as the runner-up).

Figure 2: Aileron sits within the West Arunta carbonatite province, immediately along strike from WA1's Luni — the discovery that re-rated the whole belt. (Source: ENR investor presentation, 2 Mar 2026)

4.00 — WHAT ENCOUNTER ACTUALLY HAS

From a 19 Mt system to a 120 Mt system, in one season

Encounter's maiden Aileron resource, confirmed in its 2025 Annual Report, was modest but striking on grade: 19.2 Mt at 1.74% Nb₂O₅.6 A single season of drilling later, on 21 April 2026, the company lifted the combined Inferred resource by 54% to 120 Mt at 0.77% Nb₂O₅ (0.25% cut-off), including a high-grade core of 26 Mt at 1.7% Nb₂O₅ (1.0% cut-off) across a cluster of deposits anchored by Green and Crean (Figure 3).7,8

Figure 3: Green and Emily MRE outline in plan view. (Source: ENR 22 April 2026)

Two things matter in that picture. First, the dilution of grade is real and is the heart of the bear case — a big, low-grade Inferred inventory is valued very differently from a small high-grade one. Second, and less discussed, the 26 Mt high-grade core at 1.7% is grade in the same league as Luni's higher-grade subsets, and it is exactly the material the company intends to stand up as starter pits.7,8 A project is rarely valued on its average grade; it is valued on the grade of the first thing it will mine.

Figure 4: Green Block Model in isometric view. (Source: ENR 22 April 2026)

The supporting work has kept pace. Metallurgical testwork at Green (Figure 4) has returned strong recoveries at high concentrate grades across multiple composites representing anticipated starter-pit sections.9 The company has lodged a Mining Lease application over the proposed mining, processing and infrastructure area, and sketched a conceptual site layout including processing plant, tailings storage, ponds, stockpiles, an airstrip, camp and a solar farm.10,11 These are the unglamorous artifacts of a project moving from "discovery" toward "development."

5.00 — THE VALUATION GAP

Roughly three times the value, per tonne in the ground

Here is where the "cheap" argument earns its keep. In late April 2026, with the upgraded resource freshly out, veteran resources columnist Barry FitzGerald put numbers on it: WA1 carried a market value around A$1.08 billion, Encounter about A$154 million at 27.5c, a gap of roughly A$854 million and asked whether that gap still made sense given Encounter's world-class resource scale and larger ground position.4

Figure 5: A back-of-envelope normalisation at two dates. Dividing each company's market value by its contained Nb₂O₅ (tonnes × grade) put WA1 near A$491/t and Encounter near A$167/t in late April; by late June both had drifted lower to roughly A$459/t and A$154/t. The discount didn't narrow — it held at about 3× even as Encounter's resource growth, metallurgy, mining-lease lodgement and battery MoU all landed.

Samso calculation from disclosed resources and market values: April per FitzGerald / Stockhead, 26 Apr 2026; June per market data (stockanalysis.com / Yahoo Finance, ENR A$142.6m at $0.255 on 15 Jun 2026, WA1 ~A$1.01bn mid-Jun 2026); resources per ENR & WA1 ASX disclosures. In-ground metrics ignore confidence category, metallurgy and dilution and are indicative only.

The concluding thought that should interest a value-minded reader is that the gap has not shrunk. When you look at the numbers two months on, in late June 2026, the picture barely moved. Both stocks drifted lower together (WA1 to about A$1.01 billion, Encounter to about A$143 million), so the per-tonne discount didn't close at all. It held at roughly 3×, and on an absolute per-tonne basis Encounter is fractionally cheaper than it was in April — despite the resource upgrade, the metallurgy, the mining-lease lodgement and the battery MoU all arriving in between.1,4 Good news landed; the re-rate didn't.

The market's implied logic is a "one winner" assumption: that the West Arunta produces a single developed niobium mine and it will be Luni, so WA1 deserves the premium and Encounter the scraps.4 In some ways, it does make sense, WA1 is more advanced, higher grade and higher confidence.

However, the potential error with this line of thinking is that it ignores three things Encounter Resources can point to in its valuation. Firstly, there is a resource still actively growing, second, a rare-earth and copper-gold upside across a dominant ground position, and finally, a high-grade core that doesn't need the whole 120 Mt to work.4

For context on how the market once saw the upside, in August 2025 broker Argonaut carried a 70c valuation on the stock which is multiples of where it trades today.12

Samso take A discount to WA1 is correct. The size of the discount is the debating point. When a higher-grade, more-advanced peer trades at ~3× your in-ground value, the gap can close two ways — the peer de-rates, or you prove enough to deserve a re-rate. Encounter can't control the first. Section 6 is about the second. |

6.00 — THE OTHER SIDE

Why the share price has fallenFour factors behind the decline

Encounter's share price fell from a 52-week high near $0.62 to about $0.255 by mid-June 2026. The decline is not attributable to any single announcement. As far as I can understand, there may be four separate factors account for it, and each remains a genuine risk to the investment case.

Figure 6: Three reference points over the past year: the 52-week high (~$0.62), the November 2025 placement price ($0.45), and the price in mid-June 2026 (~$0.255). Samso illustration; prices per ENR ASX placement disclosure (Oct–Nov 2025) and market data (stockinvest.us, 15 Jun 2026).

Four factors behind the decline 1. Grade dilution. As the resource grew, the average grade fell from 1.74% to 0.77% Nb₂O₅. Niobium projects are valued heavily on grade, so a larger, lower-grade resource is valued differently from a smaller, higher-grade one.6,7 2. Placement dilution. In October–November 2025 Encounter issued 54,444,444 shares at $0.45 to raise about $24.5 m (the first tranche of a $25 m placement). This increased the shares on issue and established a reference price below the earlier highs.13,14 3. Resource confidence. The entire 120 Mt resource is classified as Inferred, the lowest-confidence category under the JORC Code, and cannot yet support a development study.7,8 4. Pre-revenue status. Encounter is several years from production, and will be funding expenditure for a while to come. Its share price therefore moves with sentiment toward junior critical-minerals explorers, which has weakened since the 2024 niobium boom.1 |

Each of these factors relates to the project's current stage of development rather than to the quality of the orebody. Three of the four reasons, grade perception, resource confidence and market sentiment, would be directly affected by an upgrade of the resource from Inferred to Indicated at higher grades. That upgrade is the stated purpose of the drilling program described in the next section.

7.00 — THE CATALYST THE MARKET IS UNDERWEIGHTING

30,000 metres aimed at the one word the resource is missing

In June 2026 Encounter put two rigs on the ground as the front end of a planned ~70,000m 2026 program. What I like is the 40,00m of regional drilling chasing the next discovery which is one asset that Encounter has and WA1 Resource do not, exploration upside.

The number that matters for valuation is the 30,000 m of infill drilling across the potential starter-pit areas at Green, with an explicit purpose to upgrade the resource from Inferred to Indicated and unlock the more detailed technical studies that an Inferred resource cannot support.10,11,15

Figure 7: The infill program targets the rung the valuation is stuck on. An Inferred-to-Indicated upgrade at the high-grade starter-pit zones is the event most likely to force a re-rate of how the resource is priced. Samso illustration of ENR's stated program (ASX activity update, June 2026; mining.com.au; smallcaps.com.au).

This is important because the extra drilling should upgrade the resource to higher confidence and hopefully allow the grade to be more attractive. The infill program is aimed at the high-grade starter-pit zones as well and hence, create a dual benefit in time.

Converting Inferred to Indicated will help the project be put into the economic studies that institutions actually underwrite. It is, in plain terms, the difference between "interesting tonnes" and "a project you can value." The market is pricing the resource as Inferred today because that is what it is. The catalyst is the moment that sentence changes.

Figure 8: "Conceptual Site Layout for the Aileron Project" (processing, TSF, ponds, airstrip, camp, solar farm). (Source ENR 16 June 2026 ASX release)

Figure 9: "Aileron Magnetics (RTP) showing prospects to be tested in 2026 and major regional faults." The layout signals the explorer-to-developer shift; the magnetics map shows where the rigs are going in 2026 to test regional prospects.

Investors should look at the simple fact that upgrading the resource make the 2026 pipeline read less like a single drill-result lottery and more like a sequenced de-risking. The de-risking process will be a process that includes the infill to lift confidence, a third rig in Q3 for the geotechnical, hydrogeological and metallurgical samples that feed engineering, a mining lease already lodged, environmental baseline studies underway, and 40,000 m of regional drilling holding the blue-sky option open across niobium, REE and copper-gold.10,11,15

If even the confidence upgrade lands as intended, the most-quoted reason for the discount, "it's all Inferred" — stops being true.

Samso take — the thesis in one paragraph Encounter looks oversold not because the factual case is wrong, but because the factual case is time-limited. Typically, for investors, especially the more sophisticated versions, the grade, confidence and sentiment are the three legs of the discount. Hopefully the infill program aimed squarely at the high-grade starter-pit zones will be sufficient to knock out two of them in one campaign. The market is pricing today's Inferred resource so hopefully, the 30,000m will move the valuation up as Encounter moves its resource from inferred to indicated and beyond. I think that is the potential catalyst that will change the markets view of Encounter. The risk will come from a disappointing infill drilling result where grade continuity does not hold, a faulty Indicated upgrade (less grade, less tonnes), and a continued market depression in the commodity or the market in general. The continued decrease in gold price will create a negative general market sentiment which will put weight on the share price of a broader range of ASX companies such as Encounter Resources. |

How to read the next six months The cleanest test of this thesis is specific and public: watch for the updated Mineral Resource Estimate that carries an Indicated component at the Green starter-pit zones, and the grade it reports there. If that lands and the discount to WA1 doesn't narrow, the "oversold" read was wrong. If it lands and the gap closes, the market was simply early to sell and late to look. |

References & sources

Every project figure in this Insight is drawn from Encounter Resources' public ASX disclosures or a named third party, listed below. Company geological and site figures are referenced for insertion from the original releases rather than recreated, as the company's own diagrams are authoritative. All charts marked "Samso illustration/calculation" are our own renderings of disclosed data.

Share-price range, current price and pre-revenue/loss status — market data, ENR.AX (stockinvest.us; stockanalysis.com; Yahoo Finance), price ~$0.255 on 15 Jun 2026, 52-week high ~$0.62.

Operational momentum vs price drift — synthesised from the ENR announcement timeline below.

Niobium market structure, pricing, end-uses and supply concentration — B. FitzGerald (Garimpeiro), "Why Encounter's niobium story is more than WA1 nearology," Stockhead, 26 Apr 2026; Resources Rising Stars, Aug 2025 (US$5 bn market scale).

WA1 / Luni comparison, market values, $854 m gap, "one winner" framing, Luni 220 Mt @ 1.0% Nb₂O₅ Indicated — FitzGerald, Stockhead, 26 Apr 2026.

Niobium-anode batteries; Echion Technologies / Switch Technologies MoU (27 May 2026); CBMM backing; haul-truck trial — Kalkine, 27 May 2026; smallcaps.com.au (Jun 2024, CBMM/VW testing).

Maiden Aileron MRE 19.2 Mt @ 1.74% Nb₂O₅ — ENR 2025 Annual Report (reported via smallcaps.com.au, 17 Feb 2026).

Resource upgrade to 120 Mt @ 0.77% Nb₂O₅ (Inferred, 0.25% cut-off) incl. 26 Mt @ 1.7% (1.0% cut-off) — ENR ASX, "Aileron Resources Grow by Over 50% to 120Mt," 21 Apr 2026.

Resource detail, starter-pit intent, higher-grade subsets — ENR ASX (21 Apr 2026); smallcaps.com.au, 12 Jun 2026.

Strong metallurgical recoveries at Green — ENR ASX, "Strong Metallurgical Recoveries at Aileron – Green," 17 May 2026.

Mining Lease application; conceptual site layout (processing, TSF, ponds, airstrip, camp, solar farm) — ENR ASX activity update, June 2026; smallcaps.com.au, 12 Jun 2026.

70,000 m program: 30,000 m infill at Green (Inferred→Indicated, starter pits) + 40,000 m regional + third rig Q3 2026 (geotech/hydro/met) — ENR ASX activity update, June 2026; mining.com.au, 12 Jun 2026.

Argonaut 70c valuation on ENR — Resources Rising Stars, Aug 2025.

$25 m placement: 54,444,444 shares at $0.45 (first tranche ~$24.5 m) — Globe and Mail / TipRanks, 6 Nov 2025.

Raise context, treasury to ~$38 m — miningnews.net, 30 Oct 2025.

2026 program / catalyst framing and confidence-category logic — ENR ASX activity update (June 2026); discoveryalert.com.au; smallcaps.com.au; mining.com.au.

Announcement timeline (Feb–Jun 2026) — ENR ASX releases via stocklight.com / Market Index: "High-Grade Niobium Extends Over 4km at Green" (17 Feb), "Aileron Resources Grow by Over 50% to 120Mt" (21 Apr), "Quarterly Activities Report" (29 Apr), "Strong Metallurgical Recoveries at Aileron – Green" (17 May), "Niobium-Lithium Battery Development MOU" (26 May).

Primary sources are Encounter's ASX announcements, available on the ASX platform and the company's investor page. Where this note cites a secondary outlet, it is because that outlet aggregated or commented on the underlying ENR disclosure; readers should verify against the original release.

Depth over hype. |

This Insight is part of Samso's Sector & Commodity pillar — standalone analysis of the commodities, geology and market structures that shape the ASX small- and mid-cap resource sector. |

Not financial advice. Samso publishes research and education. This note explains the geology of tungsten skarn mineralisation in general terms; it is not a recommendation on any company or security, and deposit specifics should be checked against each company's own disclosures. Investors are expected to do their own work.

The Samso Way – Seek the Research

Here at Samso, we pride ourselves on delivering content for investors that is independent and informed by over three decades of experience in the industry. Our content is well-researched and is only created if I see merit in discussing the company's story.

Our mission is simple: cut through the noise and spotlight what matters—genuine stories, grounded insights, and real opportunity.

Our content is well-researched and is only created if the team sees merit in discussing the company or concept. Investors can explore our three core platforms:

There may be numerous paths to success in investing, but the common thread among successful individuals is that they remain committed to making informed decisions. Equip yourself with the right knowledge and tools, and you will be well on your way to achieving your financial goals.

Most importantly, investors need to be absolutely diligent in understanding their own risk-reward tolerance and capabilities. Never bite off more than you can chew. As they say, Rome wasn’t built in a day, and the Great Wall stood because it took centuries to complete.

The Samso Philosophy:

Stay curious. Stay sharp. And remember—digging deeper always uncovers the real value.

In Life, there is no such thing as a Free Lunch.

Never bite off more than you can chew is my parting comment.

Happy Investing, and the only four-letter word you need to know is DYOR.

To support our independent nature of our work, please head over to our Support Page and give us a helping hand in any of the ways listed. This is a new initiate for the Samso Platform, and it was always the concept of Samso when we started this journey in 2018.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints.

Share to Grow: Your Bonus

Samso has just released an eBook: How to Add Value to your Share Portfolio

|A lesson on geological models sought by mining companies that gives insight and an understanding of which portfolios are better - and potentially more lucrative – investments. Click here to download this eBook.|

If you find this article informative and useful, please help me share the information. I try to write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters. If you or your organisation sees the benefit of what Samso is trying to achieve and has a need to share your journey, please contact me at noel.ong@samso.com.au.

Samso is a trusted platform that equips dedicated investors with up-to-date industry knowledge and insigh0ts from top CEOs and thought leaders. By staying informed on business advancements and market trends, investors can enhance their financial decisions through a combination of expert guidance and their own research.

Samso Insights | www.samso.com.au | An Investor Lens on ASX-Listed Companies

Comments