Maritana Minerals (ASX: MRT) – Black Swan Processing Hub Scales to 2.5Mtpa | A Gold Mining Hub Takes Shape

- Noel Ong

- Jun 18

- 11 min read

Updated: Jul 9

The West Australian gold developer is targeting first production from multiple ore sources in the second half of 2027

At a Glance

Item | Description |

Company | Maritana Minerals Limited (ASX: MRT) |

Focus | Gold development — the Black Swan Processing Hub, a brownfield Carbon-in-Leach (CIL) gold plant |

Location | ~50km from Kalgoorlie, in the Western Australian Goldfields |

Key development | FEED completed; planned nameplate throughput lifted from 2.2Mtpa to 2.5Mtpa |

The plant | Repurposing the former Poseidon Nickel concentrator (acquired via merger), leaning on existing crushing and grinding infrastructure |

Throughput arc | 1.5Mtpa (PFS) → 2.2Mtpa (Feb 2026 Scoping Study) → 2.5Mtpa (FEED) |

First ore sources | Boorara, Coote and Crake open pits and the Cannon underground mine; Burbanks studies continuing |

Production ambition | ~100,000oz per annum gold producer (subject to further technical and economic study) |

Balance sheet | $229M cash plus ~$11M of listed investments |

Key contractors | GR Engineering Services (FEED / EPC); Zeal Engineering (Owner's Engineer); MineBuild Global (mining establishment and restart) |

Corporate | MD & CEO Grant Haywood; Liz Jones appointed COO from 26 August 2026 (ex-GM, Ramelius Mt Magnet regional hub) |

Approvals | Works approvals, Mine Development and Closure Proposals (MDCPs) and native vegetation clearing permits lodged and advancing |

Timeline | Construction targeted mid-2026; first production H2 2027; ore commissioning H1 FY28 |

Next steps | Capital cost review and EPC arrangements with GRES ahead of a Final Investment Decision; SAG mill removal from June 2026; approvals to grant; open-pit, underground and haulage contracts awarded late 2026 |

Maritana Minerals Limited (ASX: MRT) has delivered a comprehensive progress update earlier this month on the Black Swan Processing Hub (BSPH), located roughly 50km from Kalgoorlie in the heart of the Western Australian Goldfields.

The headline is a clean one: front-end engineering design work has lifted the planned nameplate throughput of the plant from 2.2 million tonnes per annum (Mtpa) to 2.5Mtpa, and the broader development effort has shifted visibly from the drawing board to the dirt.

Construction is targeted to commence in mid-2026, with first production from multiple ore sources flagged for the second half of 2027.

For those who have followed this story, the throughput number tells you more than it first appears. The earlier Pre-Feasibility Study contemplated a 1.5Mtpa plant. The February 2026 Scoping Study moved that to 2.2Mtpa. The FEED work has now pushed it to 2.5Mtpa. The direction of travel matters as much as the destination.

Managing Director and CEO Grant Haywood commented:

Maritana is "delighted with the substantial progress" at Black Swan. According to Haywood, the completed FEED study and the lift in nameplate throughput above 2.2Mtpa "materially improves the Project's production capacity," with site activity ramping up quickly and key approvals advancing. Combined with the company's de-risking initiatives across infrastructure, accommodation and power, he says Maritana is well positioned for a mid-2026 construction start and first production from multiple ore sources in the second half of 2027, with the team focused on delivering Black Swan as a cornerstone asset.

Highlights – The Path to a Gold Mining Story

Engineering and Design

The Front-End Engineering Design (FEED) phase has been completed, with the report prepared by GR Engineering Services (GRES) now submitted for review. This is the engine room of the update. GRES has identified the potential to run the plant at 2.5Mtpa rather than the 2.2Mtpa carried in the Scoping Study, based on a closer look at the available ore sources and the capability of the existing crushing and grinding infrastructure already standing at Black Swan.

Figure 1: Existing infrastructure at Black Swan (Source: MRT Webiste)

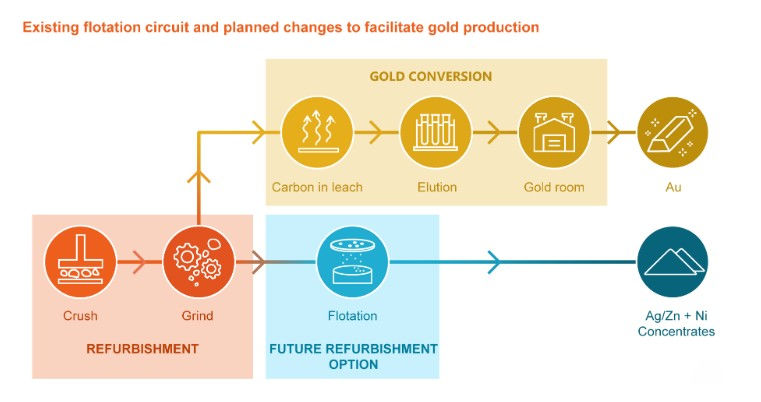

That last point is the crux of the Black Swan thesis. Maritana did not build this plant from scratch — it inherited a brownfield concentrator through the Poseidon Nickel merger and is repurposing it into a gold Carbon-in-Leach (CIL) operation (Figure 1). Being able to dial throughput higher by leaning on existing comminution capacity is exactly the kind of latent optionality that brownfield assets are supposed to deliver. The company frames the uplift as supportive of its stated ambition to become a ~100,000-ounce-per-annum gold producer, though it is careful - correctly - to flag that this remains subject to further technical and economic study. (Figure 2).

Figure 2: Flotation circuit and planned changes (Source: MRT Webiste)

Capital Cost

Here is where Samso readers should keep their eyes open. Maritana has been candid that process plant capex is likely to rise in line with both the throughput uplift and broader inflationary pressures. The capital implications of the 2.5Mtpa design are still being assessed within the FEED review, and a revised estimate - together with any impact on the mine plan - will come to the market in due course.

The company says it is actively reviewing all capital items to identify cost reductions, defer expenditure beyond first gold, and explore separate financing arrangements for certain items. That is a sensible posture, but it is also the open question of this announcement. More tonnes are good. The cost of buying those tonnes is the number that will ultimately decide whether the project economics improve or merely get bigger.

Site Survey and Digital Modelling

A comprehensive LiDAR (Light Detection and Ranging) survey of the site has been completed, and the resulting point-cloud data used to build an accurate as-built digital model of the existing brownfield infrastructure. This is genuine de-risking, not window dressing. The single biggest execution risk on a brownfield refurbishment is the clash between new and old infrastructure that nobody mapped properly. An accurate digital twin reduces the chance of nasty surprises during detailed design and construction.

ROM Pad Design

Maritana has finalised the design of an enlarged Run-of-Mine (ROM) pad, sized to take ore from quad side-tipping road trains and to provide substantially more stockpiling capacity. The intent is to support ore blending and optimise mill feed — important when you are pulling from multiple deposits of varying grade and metallurgy into a single hub.

Approvals and Permitting

Works are progressing under existing approvals attached to the mining leases and the previous 2022 Poseidon Nickel feasibility study. For the new areas, the key regulatory approvals — works approvals, Mine Development and Closure Proposals (MDCPs), and native vegetation clearing permits — have been lodged and are advancing through assessment. Approvals are the quiet risk on every WA development timeline, so seeing them lodged and moving is a tick in the right box.

Owner's Engineer and Site Mobilisation

Zeal Engineering, a Western Australian firm with greenfield and brownfield experience, has been appointed as Owner's Engineer to strengthen technical oversight through construction. On the ground, two Site Senior Executives (SSEs) and an OHS Manager have been appointed, clean-up and legacy equipment removal is underway, and the removal of the Semi-Autogenous Grinding (SAG) mill — for refurbishment or potential replacement — is scheduled to begin in June 2026.

Accommodation

The accommodation strategy supports a hub-and-spoke model. A permanent 60-room camp (scalable to 120 rooms) is being designed at Black Swan, with a temporary camp bridging the gap during construction. Concurrently, Maritana is acquiring a central Kalgoorlie property that already carries development approval for around 50 rooms, with settlement expected in the June 2026 quarter. Hotel accommodation in Kalgoorlie is covering drilling and operational-readiness activity in the interim. Unglamorous, but in a labour-constrained Goldfields, beds are leverage.

Power, Water and Drilling

Western Power has commenced grid connection studies, with approvals expected next quarter, and the diesel backup power station design is complete and right-sized for redundancy. On water, Western Groundwater and Flow Water Services have been engaged for studies and bore field refurbishment. Sterilisation and geotechnical drilling has commenced across the new infrastructure areas — the CIL circuit, power station and tailings storage facility — to lock in detailed design and final siting.

Mining Operational Readiness

This is the other half of the equation, and it is easy to overlook when the plant grabs the headlines. A plant with no feed is an expensive ornament. Maritana has appointed MineBuild Global to oversee the establishment and restart of the Boorara Open Pit, the Coote and Crake Open Pits, and the development of the Cannon underground mine — the first three key ore sources for Black Swan. Contract tendering for open pit, underground and haulage services has commenced, with awards targeted for late H2 2026 to support mining starting in early 2027. Technical studies for the initial operations are complete, while work on the Burbanks open pit and underground continues.

Corporate

On the leadership front, Maritana has appointed Elizabeth (Liz) Jones as Chief Operating Officer, commencing 26 August 2026. Jones brings more than three decades of underground and open pit experience, most recently as General Manager of Ramelius Resources' Mt Magnet operations, where she oversaw the establishment of a regional processing hub — directly relevant experience for what Maritana is trying to build.

And then there is the balance sheet: a $229M cash balance plus around $11M of listed investments. For a developer at this stage, a funding position of this size is the difference between dictating the pace and being dictated to.

Next Steps

Maritana has set out a clear list of near-term priorities: finalising the EPC and reimbursable contract arrangements with GRES and completing the capital cost review ahead of a Financial Investment Decision; progressing the lodged approvals through to grant; completing the SAG mill removal and confirming the refurbishment-versus-replacement pathway; advancing accommodation and site earthworks; finalising the water strategy; pushing toward full construction with ore commissioning targeted for H1 FY28; and awarding the open pit, underground and haulage contracts in late 2026.

Figure 3: Key Milestones (Source: ASX Presentation)

Samso Concluding Comments

Maritana Minerals is simply going through its paces, and investors need to take advantage of the "resting" of the gold hype. The consensus in the market is that the fundamentals are all pointing to higher gold prices in the future. The fact that should not deter investors from considering Maritana as a potential investment idea.

Look out for our Samso Insights on the Gold Path in 2026 and beyond, which will be coming out soon.

There is probably going to be a period of no single transformational catalyst, no maiden resource, no bonanza drill hit, no surprise takeover. Instead what the market is going to see is a methodical list of de-risking steps being knocked over one by one: survey done, ROM pad designed, approvals lodged, Owner's Engineer appointed, SSEs on site, camps being secured, power and water progressing, mining contractor engaged, and a COO with hub-building pedigree on the way.

For investors who understand mine development, this is what progress actually looks like. It is what I call the "Boring" stage. Look at this a a period where you can get on the bandwagon again or for those that have not, to get a second chance to get on the journey.

The throughput uplift to 2.5Mtpa is a positive, and the scaling arc of 1.5Mtpa at PFS, 2.2Mtpa at Scoping Study, now 2.5Mtpa at FEED does indicate an asset that keeps offering more as the engineering deepens. That is the brownfield optionality thesis playing out in real time, and it is the encouraging signal in this release.

What readers should get from this Samso News is our aim to separate signal from noise, and the noise to watch here is capital. Maritana has been refreshingly upfront that capex is likely to rise with both the bigger plant and inflation. More tonnes only creates value if the cost of delivering them does not eat the upside. The revised capital estimate, when it lands, is the number that matters. A $229M cash position buys patience and optionality, but it does not make the capex question disappear.

The other thing worth holding in mind is execution sequencing. Maritana is building a plant and standing up multiple mines and securing accommodation and locking in power and water, all at once, all on a mid-2026-to-2027 timeline. The hub-and-spoke model works on paper but the challenge, as ever in this game, is converting a tidy plan into commissioned tonnes and poured gold without timeline slip or budget blowout.

In my our opinion, the market will now be waiting for two things: the revised capital number, and the first sign of steel going up. Time, as always, will be the key determinant of whether the ~100koz aspiration becomes a production reality or remains an aspiration.

About Maritana Minerals Limited

Maritana Minerals Limited (ASX: MRT) — formerly Horizon Minerals, renamed in April 2026 — is an emerging gold developer and producer advancing a portfolio of assets across Western Australia's prolific Eastern Goldfields (Figure 4). Following its transformational merger with Poseidon Nickel and the subsequent Gordons acquisition, the company holds a mineral resource base of around 1.88Moz of gold (34.32Mt at 1.7 g/t Au) across roughly 1,386 km² of tenure in some of Australia's most productive gold belts.

Maritana Minerals holds a 100% interest in gold projects in the Kalgoorlie and Coolgardie regions, including the 428,000oz Boorara project and 1,372,000oz in satellite projects in close proximity.

At the centre of Maritana's strategy is the Black Swan Processing Hub, located approximately 50km from Kalgoorlie. Acquired as a brownfield concentrator through the Poseidon Nickel merger, the plant is being refurbished and converted into a gold Carbon-in-Leach (CIL) operation, with front-end engineering design lifting planned nameplate throughput to 2.5Mtpa.

The hub is designed to provide centralised processing for ore drawn from multiple company-owned deposits — including the Boorara, Coote and Crake open pits and the Cannon underground mine — under a hub-and-spoke model, with construction targeted for mid-2026 and first production in the second half of 2027. The company's stated ambition is to become a standalone gold producer of around 100,000 ounces per annum.

Figure 4: Location of Maritania's Projects (Source: ASX Presentation)

The Samso Way – Seek the Research

Here at Samso, we pride ourselves on delivering content for investors that is independent and informed by over three decades of experience in the industry. Our content is well-researched and is only created if I see merit in discussing the company's story.

Our mission is simple: cut through the noise and spotlight what matters—genuine stories, grounded insights, and real opportunity.

Our content is well-researched and is only created if the team sees merit in discussing the company or concept. Investors can explore our three core platforms:

There may be numerous paths to success in investing, but the common thread among successful individuals is that they remain committed to making informed decisions. Equip yourself with the right knowledge and tools, and you will be well on your way to achieving your financial goals.

Most importantly, investors need to be absolutely diligent in understanding their own risk-reward tolerance and capabilities. Never bite off more than you can chew. As they say, Rome wasn’t built in a day, and the Great Wall stood because it took centuries to complete.

The Samso Philosophy:

Stay curious. Stay sharp. And remember—digging deeper always uncovers the real value.

In Life, there is no such thing as a Free Lunch.

Never bite off more than you can chew is my parting comment.

Happy Investing, and the only four-letter word you need to know is DYOR.

To support our independent nature of our work, please head over to our Support Page and give us a helping hand in any of the ways listed. This is a new initiate for the Samso Platform, and it was always the concept of Samso when we started this journey in 2018.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints.

Share to Grow: Your Bonus

Samso has just released an eBook: How to Add Value to your Share Portfolio

|A lesson on geological models sought by mining companies that gives insight and an understanding of which portfolios are better - and potentially more lucrative – investments. Click here to download this eBook.|

If you find this article informative and useful, please help me share the information. I try to write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters. If you or your organisation sees the benefit of what Samso is trying to achieve and has a need to share your journey, please contact me at noel.ong@samso.com.au.

Samso is a trusted platform that equips dedicated investors with up-to-date industry knowledge and insigh0ts from top CEOs and thought leaders. By staying informed on business advancements and market trends, investors can enhance their financial decisions through a combination of expert guidance and their own research.

Samso News | www.samso.com.au | An Investor Lens on ASX-Listed Companies

Comments