Unpacking the Lux Copper IPO (ASX: LUX)

- Noel Ong

- 42 minutes ago

- 11 min read

The company is a copper-zinc explorer that sits in the best mining address in the world

AT A GLANCE |

Company Name: Lux Copper Corp. Ltd Proposed ASX Code: LUX Raise: $8m – $15m @ $0.25/share (32m – 60m shares) Indicative Market Cap: ~$23.2m – $30.2m Prospectus lodged: 3 June 2026 | Offer closes: 25 June 2026 Expected ASX quotation: 17 July 2026 What you are looking at: A copper-zinc explorer whose entire story sits in one of the better mining addresses in the world — Alaska's Ambler district, home to Teck's Red Dog mine and Trilogy Metals' Arctic and Bornite deposits. Through its Alaskan subsidiary, Lux holds 100% of two projects: the flagship Baird (41 claims, ~2,600 ha) and the district-scale Ambler (368 claims). Baird already carries genuinely high-grade historical copper hits. The raise funds a maiden drill program at Baird and first-pass work at Ambler. Lead manager is Canaccord Genuity The strongest leg: The grade and the neighbourhood. Historical drilling at Baird's Omar prospect returned intercepts like 37.7m @ 2.45% Cu (including 4.9m @ 10.23% Cu) and 4.9m @ 9.83% Cu — high-grade copper, in a Fraser-Institute top-12 jurisdiction, next door to world-class deposits, with copper trading near record highs in 2026.<br> The points of friction: No JORC resource on either project — this is a drilling story. The ground is remote, fly-in Alaskan terrain with a short field season and real permitting/claim-maintenance obligations. And as ever with a pre-revenue explorer, the rig has to deliver. |

01/ The 60-Second Pitch

Lux Copper Corp. Ltd (proposed ASX: LUX) is a Western Australian-incorporated explorer with a wholly American asset base: through its Alaskan subsidiary Lux Copper LLC, it owns 100% of two copper-zinc projects in the Northwest Arctic Borough of Alaska. It's raising $8m–$15m at $0.25 to drill them.

The pitch for the Lux Copper IPO is built on two things that genuinely matter in exploration: grade and address. On address, Lux's ground sits in the Ambler Mining District — one of the most prospective base-metals belts in North America, anchored by Teck Resources' Red Dog (one of the world's great zinc mines) and the Lik deposit, plus Trilogy Metals' Arctic and Bornite copper deposits (Figure 1). Alaska itself was rated twelfth globally for mining investment attractiveness by the Fraser Institute in 2025: low sovereign risk, established mining law, a top-tier jurisdiction.

Figure 1:Location of Projects within Alaska, United States (Source: IPO Prospectus)

On grade, the flagship Baird Project is the reason to look. Historical drilling at its Omar prospect returned the kind of numbers that make copper geologists sit up — 37.7m at 2.45% Cu including 4.9m at 10.23% Cu, a separate 4.9m at 9.83% Cu including 3.3m at 12.12% Cu, and rock chips running above 30% copper and 20% zinc. Those are high-grade results, and Lux's first job after listing is a maiden drill program to test and extend them.

The second project, Ambler, is a much larger land position — 368 claims across the Ambler metallogenic belt — held for early-stage, district-scale optionality rather than near-term drilling.

What you are buying, as always with this kind of float, is not a resource. There's no JORC estimate on either project yet; that's the whole point of the raise. Lux is a high-grade drilling story in a great neighbourhood — with all the remoteness, permitting and execution risk that exploring in Arctic Alaska implies.

02/ Lux Copper IPO Snapshot

Table 1: IPO Snapshot

Item | Detail |

Company | Lux Copper Corp. Ltd (ACN 682 515 304) |

Proposed ASX Code | LUX |

Offer Price | $0.25 per share |

Raise (min / max) | $8.0m / $15.0m (32,000,000 / 60,000,000 shares) |

Indicative Market Cap (min / max) | ~$23.23m / ~$30.23m |

Existing Shares on Issue | 60,912,468 |

Shares on Issue at Admission (min / max) | 92,912,468 / 120,912,468 |

Free Float | ~42% (not less than 20%) |

Lead Manager | Canaccord Genuity (Australia) Limited |

Co-Managers | GBA Capital; Peloton Capital |

Independent Geologist | Piton Exploration LLC (Palmer, Alaska) |

Existing Cash (Prospectus Date) | $994,372 |

Lodgement / Open / Close / Quotation | 3 June / 11 June / 25 June / 17 July 2026 |

Underwritten? | No |

Assets | 100% Baird Project & Ambler Project, Northwest Arctic Borough, Alaska |

03 / Capital Structure & Dilution

The dilution here is moderate and scales with how much gets raised. Existing holders own 60.9 million shares; depending on subscription, the company ends up with either ~92.9m shares (minimum) or ~120.9m (maximum). That puts existing holders at roughly 66% at the minimum raise and about 50% at the maximum — i.e. new money takes between a third and a half of the company. Not a wash-out, but at the top end the public is buying close to half the register.

Table 2: Capital Structure on Admission

Security | Min subscription | Max subscription |

Existing shares | 60,912,468 | 60,912,468 |

Public Offer shares | 32,000,000 | 60,000,000 |

Total shares on issue | 92,912,468 | 120,912,468 |

Options (Lead Manager / Adviser / Board) | 27,500,000 | 27,500,000 |

Performance Rights | 8,000,000 | 10,000,000 |

Market capitalisation | ~$23.23m | ~$30.23m |

The options and rights stack is worth a note. On top of the shares there are 27.5 million options (1.5m to the Lead Manager, 0.5m to the Adviser, 9m to board and management, plus the 16.5m existing) and 8–10 million performance rights to board and management. That's a meaningful overhang of potential future dilution if it all vests and exercises — standard for a float of this type, but it's there.

One quietly interesting number: strip the cash out of the market cap and the implied enterprise value lands around $14m at either end of the raise (because raising more simply adds more cash). So the market is being asked to value the two Alaskan projects at roughly $14m — modest for high-grade ground next to world-class deposits, which is the bull's framing, but also a reminder that you're paying for drill targets, not a defined resource. Free float is expected to be ~42%.

04/ Use of Funds

This is a tidy, exploration-led budget — most of the money goes into the ground, which is exactly what you want.

Table 3: Use of Funds (2 years)

Use of funds | Min ($) | % | Max ($) | % |

Exploration expenditure | 6,100,000 | 68% | 12,500,000 | 78% |

Costs of the Offers | 903,235 | 10% | 1,332,444 | 8% |

Directors' fees | 400,000 | 4% | 400,000 | 3% |

Working capital | 1,591,137 | 18% | 1,761,928 | 11% |

Total funds available | 8,994,372 | 100% | 15,994,372 | 100% |

Total includes ~$0.99m of existing cash. Exploration figure combines Year 1 and Year 2.

Putting 68–78% of available funds into exploration is at the strong end for a float this size, and the weighting tilts harder to drilling as the raise grows (Year 2 exploration roughly doubles between the minimum and maximum cases). Costs of the offer (~8–10%) are typical for a non-underwritten small-cap, and directors' fees of $400k over two years are lean. The prospectus is explicit that the raise funds roughly two years of activity, and that — being pre-revenue — Lux will need to raise again down the track.

5/ The Projects

Table 4: Project Portfolio

Project | Claims | Area | Stage | Why it matters |

Baird | 41 | ~2,600 ha | Maiden drilling | High-grade historical copper at the Omar prospect; the flagship |

Ambler | 368 | District-scale | Reconnaissance | Large position in the Ambler belt, near Trilogy's Arctic & Bornite |

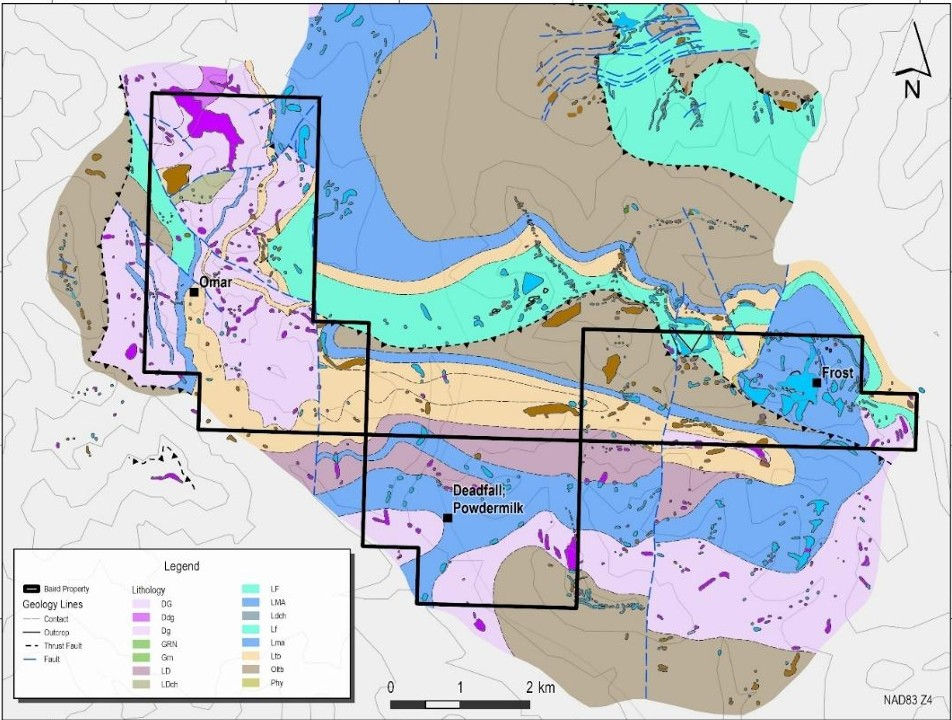

5.1 Baird — The Flagship

Baird is where the value case lives. It's a compact, 41-claim project (~2,600 ha) in the eastern Baird Mountains, and its Omar prospect carries the high-grade copper that makes the whole story. Historical drilling there (reported by Freeman, 2013) returned standout intercepts:

BC-06: 37.7m @ 2.45% Cu, including 4.9m @ 10.23% Cu

BC-05: 4.9m @ 9.83% Cu, including 3.3m @ 12.12% Cu

BC-08: 9.8m @ 2.15% Cu

plus intervals around 3.46% Cu and 2.78% Cu, and zinc up to 2.77m @ 8.11% Zn

Historical surface sampling along the Omar–Frost–Deadfall corridor threw up rock chips exceeding 30% copper and 20% zinc, with silver credits. That's high-grade by any measure. The catch is the usual one: these are historical, selective, target-focused results, not a JORC resource — so Lux's maiden drill program is about validating and extending what's there, not banking it. Baird was acquired under the Baird Acquisition Agreement, so there's vendor and counterparty performance to rely on (a flagged contractual risk).

Figure 2: Baird Project geology map (Source: IPO Prospectus )

5.2 Ambler — The District-Scale Option

Ambler is the bigger but earlier play: 368 claims across the Ambler metallogenic belt, the same belt that hosts Trilogy Metals' Arctic (a high-grade copper-zinc-lead-silver-gold VMS deposit) and Bornite (copper). Work here is first-pass — reconnaissance fieldwork, compilation, geophysics — rather than drilling in the near term. Treat it as cheap district-scale optionality: a large foothold in a proven belt, with the blue-sky that comes from being early, and the uncertainty that comes with it.

6/ The Exploration Budget

The spend is genuinely drilling-led. Across the two years, exploration runs $6.1m (minimum) to $12.5m (maximum), and the prospectus earmarks it for the things that move an exploration story: access and claim maintenance, geophysics, soil sampling and fieldwork, drilling and assays, and metallurgical test work. The early emphasis is the maiden drill campaign at Baird to test the Omar copper, with reconnaissance at Ambler running alongside. At the maximum raise, Year 2 exploration jumps to $6.5m — that's the follow-up-drilling scenario, where a good first season gets pressed home.

7/ The Board & Related Parties

Table 5: Board & Management

Name | Role | Note |

Mark Williams | Non-Executive Chair | Largest individual holder (~14.3% pre-IPO); associated with the chair's private group used as the registered office |

Simon Dahrouge | Non-Executive Director | Nil shares at prospectus date; connected to the Dahrouge geological family, which provides services |

Troy Cavanagh | Non-Executive Director | ~4.4% pre-IPO |

James Warren | Chief Executive Officer | Runs the company day-to-day |

At the prospectus date, the directors and associates held roughly 18.7% of the company (Williams ~14.3%, Cavanagh ~4.4%), which dilutes down on admission. The structure is a non-executive board chaired by Williams with a CEO (Warren) driving operations.

8/ The Market — Copper, Zinc and Alaska

The macro case is strong and topical. Copper has been trading near record highs through 2026 on a structural supply-demand squeeze — electrification, grid build-out and data-centre demand against a thin pipeline of new mines — and it's squarely a critical mineral for both the US and allied supply chains. Zinc, the other half of the story, is the metal that built Red Dog into one of the world's largest mines, just up the belt.

Then there's the jurisdiction. Alaska is a genuine top-tier mining address — twelfth globally on the Fraser Institute's 2025 attractiveness ranking, with established mining law and low sovereign risk — and the Ambler district's pedigree (Red Dog, Lik, Arctic, Bornite) is exactly the kind of neighbourhood an explorer wants to be drilling in.

The counterweight, and it's a real one, is remoteness and access. This is fly-in Arctic exploration — the prospectus flags an Aircraft Charter Agreement for getting to the ground — with a short summer field season, mandatory annual claim-maintenance spending, and exploration permits granted for fixed terms with reporting obligations. The Ambler district's access and permitting have been a long-running, politically sensitive story in their own right. The grade and the geology are there; getting at them, season after season, is the operational reality investors are signing up for.

9/ The Risks / Points of Friction

No JORC resource. Both projects are pre-resource; the historical Baird hits are encouraging but unproven under modern standards. This is a drilling story.

Pre-revenue, will raise again. Funded for ~2 years; as a pre-revenue explorer, further capital will be needed, with the usual dilution risk.

Remote, seasonal, permit-dependent. Fly-in Arctic Alaska, short field season, annual claim-maintenance obligations, and permitting/access risk in the Ambler district.

Contractual risk. Reliance on the Baird Acquisition Agreement vendors and the Aircraft Charter Agreement counterparties.

Dilution / overhang. New money takes ~34–50% of the company depending on raise, plus 27.5m options and 8–10m performance rights as future dilution.

Single-commodity-region concentration. The whole story rides on two adjacent Alaskan projects and the copper price.

Samso Concluding Comments

The Lux Copper IPO is a clean, high-grade exploration story with a genuinely good address. There are no promotive resource to bank, no production, no revenue but it is in sa great neighbourhood, a flagship project with eye-catching historical copper grades, and a budget built to drill.

There is a lot to like about this exploration story. The Baird grades, 37.7m at 2.45% Cu including 4.9m at over 10% Cu, rock chips above 30% copper are good historical results that justify a drill program, not just nearology speak but indicative of the presence of potential.

The Ambler district is a proven base-metals belt with world-class neighbours. I like Alaska as it is a well known top-tier jurisdiction. Copper and zinc are the right commodities at the right time, however, zinc has been a stop and start dance which has not been too electric for the market.

The challenges are just as real, and they cluster around stage, location and structure. Nothing is a resource yet. The ground is remote, seasonal and permit-dependent, which makes exploration slower and costlier than it looks on a map. The register and service arrangements carry a related-party flavour that deserves a careful read. And like every explorer, Lux will be back for more capital before this is done.

The natural thing to watch, as always, is the maiden drill program at Baird — whether the rig confirms and extends the Omar copper, and whether a good first Alaskan season can be pressed into something that grows toward a maiden resource. If it does, the combination of grade, district and copper price is a compelling one. If it doesn't, this is a remote, capital-hungry exploration play like any other. High grade, great address, real execution risk and the drill core will tell the story.

The Samso Way – Seek the Research

Here at Samso, we pride ourselves on delivering content for investors that is independent and informed by over three decades of experience in the industry. Our content is well-researched and is only created if I see merit in discussing the company's story.

Our mission is simple: cut through the noise and spotlight what matters—genuine stories, grounded insights, and real opportunity.

Our content is well-researched and is only created if the team sees merit in discussing the company or concept. Investors can explore our three core platforms:

There may be numerous paths to success in investing, but the common thread among successful individuals is that they remain committed to making informed decisions. Equip yourself with the right knowledge and tools, and you will be well on your way to achieving your financial goals.

Most importantly, investors need to be absolutely diligent in understanding their own risk-reward tolerance and capabilities. Never bite off more than you can chew. As they say, Rome wasn’t built in a day, and the Great Wall stood because it took centuries to complete.

The Samso Philosophy:

Stay curious. Stay sharp. And remember—digging deeper always uncovers the real value.

In Life, there is no such thing as a Free Lunch.

Never bite off more than you can chew is my parting comment.

Happy Investing, and the only four-letter word you need to know is DYOR.

To support our independent nature of our work, please head over to our Support Page and give us a helping hand in any of the ways listed. This is a new initiative for the Samso Platform, and it was always the concept of Samso when we started this journey in 2018.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints.

Share to Grow: Your Bonus

Samso has just released an eBook: How to Add Value to your Share Portfolio

|A lesson on geological models sought by mining companies that gives insight and an understanding of which portfolios are better - and potentially more lucrative – investments. Click here to download this eBook.|

If you find this article informative and useful, please help me share the information. I try to write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters. If you or your organisation sees the benefit of what Samso is trying to achieve and has a need to share your journey, please contact me at noel.ong@samso.com.au.

Samso is a trusted platform that equips dedicated investors with up-to-date industry knowledge and insigh0ts from top CEOs and thought leaders. By staying informed on business advancements and market trends, investors can enhance their financial decisions through a combination of expert guidance and their own research.

Samso News | www.samso.com.au | An Investor Lens on ASX-Listed Companies

Comments