Looking for Diamonds - Are they still worth looking for?

- Noel Ong

- Feb 14, 2020

- 16 min read

Updated: Sep 30, 2025

Investors all know about the value of diamonds and how much these elusive stones cost or are worth. In reality, that value is the perceived value of diamonds. I would wager that most of those investors would not realise that it is a controlled commodity, and hence the price is effectively artificial. What is interesting is also that it is one of the most challenging and most expensive product to go looking for, even with today’s technology. The last hurrah for diamonds in Australia would have to be in the early 1990s, and it is rare as hen’s teeth since that period of excitement. I had the privilege to have worked during that time and with a company that had the budget to do some real stuff, Ashton Mining Limited (taken over by Rio Tinto in the early 2000s).

There is no doubt that there is no shortage of these stones, especially the white ones (hence my fascination with coloured gemstones). However, the fact is that it is not that easy to find them and then prove it up for mining makes these stones somewhat “rare”.

The diamond formation process is one that can be a tease. Diamonds are chemically unstable in normal conditions as the metastable state is in the form of graphite. It is for this reason that diamonds need to be emplaced on the surface quickly (In a geological sense). Otherwise, it will change to a “non-diamond” form. Hence, the quickest way for this process to happen is to get delivered by a volcanic system that can allow magma (liquid-like rock material from deep within our Earth mantle) to rise to the surface.

What are the source rocks for Diamonds?

To date, there are two types of rocks where you can find diamonds. They are called Kimberlites and Lamproites. There other hybrids but they are typically some combinations of Kimberlitic and Lamproitic.

According to old faithful Wikipedia,

Kimberlite is an igneous rock, which sometimes contains diamonds. It is named after the town of Kimberley in South Africa, where the discovery of an 83.5-carat (16.70 g) diamond called the Star of South Africa in 1869 spawned a diamond rush and the digging of the open-pit mine called the Big Hole. Previously, the term kimberlite has been applied to olivine lamproites as Kimberlite II, however this has been in error. Kimberlite occurs in the Earth’s crust in vertical structures known as kimberlite pipes, as well as igneous dykes. Kimberlite also occurs as horizontal sills.[2] Kimberlite pipes are the most important source of mined diamonds today. The consensus on kimberlites is that they are formed deep within the mantle. Formation occurs at depths between 150 and 450 kilometres (93 and 280 mi), potentially from anomalously enriched exotic mantle compositions, and they are erupted rapidly and violently, often with considerable carbon dioxide[3] and other volatile components. It is this depth of melting and generation that makes kimberlites prone to hosting diamond xenocrysts. Despite its relative rarity, kimberlite has attracted attention because it serves as a carrier of diamonds and garnet peridotite mantle xenoliths to the Earth’s surface. Its probable derivation from depths greater than any other igneous rock type, and the extreme magma composition that it reflects in terms of low silica content and high levels of incompatible trace-element enrichment, make an understanding of kimberlite petrogenesis important. In this regard, the study of kimberlite has the potential to provide information about the composition of the deep mantle and melting processes occurring at or near the interface between the cratonic continental lithosphere and the underlying convecting asthenospheric mantle.

Lamproite is an ultrapotassic mantle-derived volcanic or subvolcanic rock. It has low CaO, Al2O3, Na2O, high K2O/Al2O3, a relatively high MgO content and extreme enrichment in incompatible elements.

Lamproites are geographically widespread yet are volumetrically insignificant. Unlike kimberlites, which are found exclusively in Archaean cratons, lamproites are found in terrains of varying age, ranging from Archaean in Western Australia, to Palaeozoic and Mesozoic in southern Spain. They also vary widely in age, from Proterozoic to Pleistocene, the youngest known example being 56,000 ± 5,000 years old.

Lamproite volcanology is varied, with both diatreme styles and cinder cone or cone edifices known.

The economic significance of lamproite became known with the discovery of Ellendale E4 and E9 lamproite pipes and better known 1979 discovery of the Argyle diamond pipe in Western Australia. This discovery led to the intense study and re-evaluation of other known lamproite occurrences worldwide; previously only kimberlite pipes were considered economically viable sources of diamonds.

The Argyle diamond mine remains the only economically viable source of lamproite diamonds. This deposit differs markedly by having a high content of diamonds but low quality of most stones. Research at Argyle diamond have shown that most stones are of E-type; they originate from eclogite source rocks and were formed under high temperature ~1,400 °C (2,600 °F). The Argyle diamond mine is the main source of rare pink diamonds.

Olivine lamproite pyroclastic rocks and dikes are sometimes hosts for diamonds. The diamonds occur as xenocrysts that have been carried to the surface or to shallow depths by the lamproite diapiric intrusions.

The diamonds of Crater of Diamonds State Park near Murfreesboro, Arkansas are found in a lamproite host.

Do all Kimberlites and Lamproites have Diamonds?

Not all Kimberlites or Lamproites are diamond-bearing. There are considerable complexities that define whether the source rock has diamonds or not but let’s keep it simple. Diamonds form in a specific region in the Earth’s mantle. The temperature and pressure levels are one of the significant participants, and hence when the magma passes or originates from this region, it will sample diamonds. The endowment will depend on the rate and how mature the magma is when it reaches the surface.

The schematic diagram below shows some variants of factors that affect whether the source rock contains diamonds. There are many forms of Kimberlites, and I have included this article which I think is a good description of what I am talking about, Diamonds_Kimberlites and Lamproites.

What is apparent is that they do form in clusters, and when they are of the same age, the presence of one diamond-bearing pipe will most likely mean that there are more to be found. Similarly, the presence of kimberlite or lamproite from that geochemistry will have diamonds. However, this theory is not an exact science, which is why when you find microdiamonds or a macro-diamond in exploration, you excited. This discovery means that the potential kimberlitic or lamproitic field is carrying that kind of chemistry. In term of exploration, we get excited if we find indicator minerals from that region of chemistry, but if you find diamonds, that is as close to a sure thing as you can get for diamond exploration.

In reality, to find that pipe bearing the diamonds is not even close to a sure thing as in most cases, you have to deal with drilling all the potential pipes and the likelihood the pipe is covered or weathered. Diamond exploration is one of the hardest to achieve success, in my opinion. I would go as far as to say that it is the hardest in the space that I have been in over my years of exploration. The rate of success is pretty low, and it’s expensive. Projects take a long time because the risk/reward ratio is typically low. However, the payoff is significant when you do find it.

In my previous Insight, The Webb Project: GeoCrystal Limited – The Next Diamond Story and Yellow Diamonds – A Gap in the Diamond market, I have made several mentions about this particular issue of high expenditure and lack of success in this sector.

Is there anyone looking for Diamonds?

Since the 1990s, there has not been any real exploration in Australia. However, it appears that the TSX (Toronto Stock exchange) companies have been active and of they are probably the only group that can be said to be active diamond explorers. The amount of activity is probably due to the well endowed North-West Territories of Canada. It is home to the massive Diavik Mine (8 million carats annually) and the Ekati Mine (7.5 million carats). Both these mines are still in production.

In researching this Insight, I am amazed to find that there is a long list of diamond explorers in the TSX (Toronto Stock Exchange). There is a long list of diamond producers as well. I must admit that my knowledge of this sector is decades behind, and I put this to the fact that there is no diamond action here in Australia. The only company that comes to mind is Lucapa Diamond Company Limited (ASX: LOM) and Gibb River Diamonds Limited (ASX: GIB). The diagram below shows gem-quality diamond production up to 2018. As someone had pointed out in Linkedln, Australia is missing from that list :-). I agree that this is inaccurate and I am not sure why they have left Australia out. Maybe they are talking about gem-quality stones.

The issues with this sector are that funding is challenging. I would think that the Canadians understand this sector better with so many producing mines. However, I do hear that the explorers are finding it hard to source funds as well. I know that Gibb River is currently looking for funds, but I am not sure about the progress. I would think that it is not going to be easy with the state of the diamond market.

Lucapa is one that is mining and admittedly, I have not followed it other than reading the news — looking at their share price, which is at an all-time low of AUD$0.13. What this means is anyone’s guess. For a miner, it is always hard to make a decision based on their share price. I am suspecting that this is a reflection of the market price of the stones at this moment.

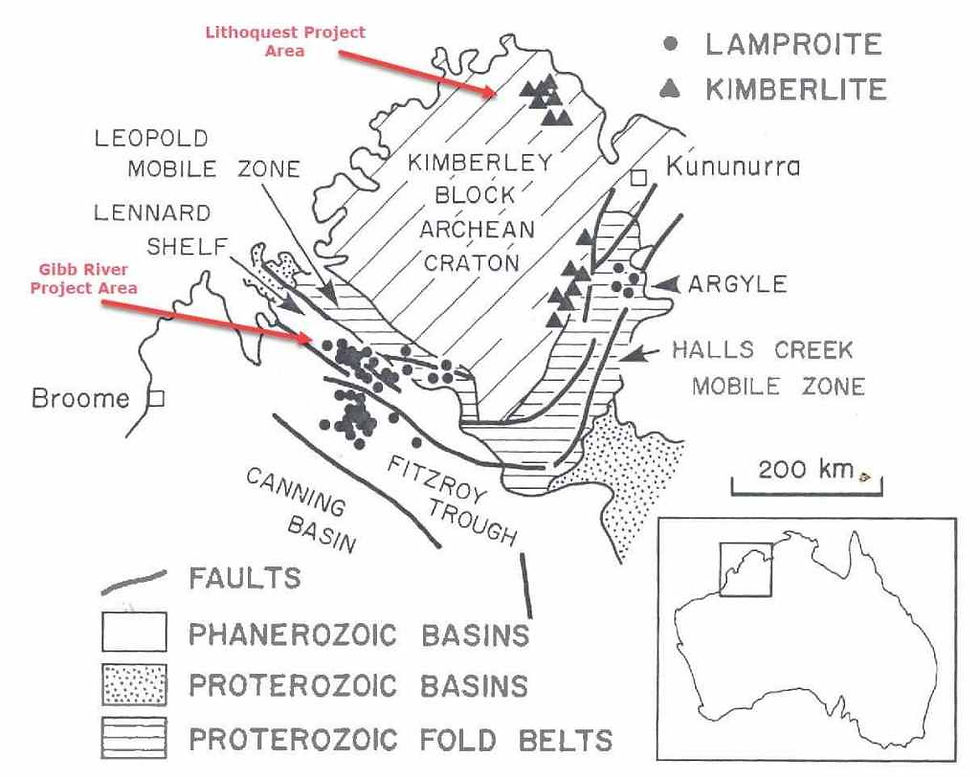

There is one Canadian company that is doing lots of work in Australia, but Australian doesn’t get a look at is Lithoquest Diamond Inc (TSX-V: LDI). They have an excellent project up in the Kimberley region of Western Australia. To date, they have found a Kimberlite field and drilled one or two of them. One microdiamond has been found although it is separate to the known Kimberlite field. For a diamond tragic like me, this is exciting as this area has not been worked on previously and is considered the ideal place to locate these pipes.

This story reminds me of the Merlin Diamond Project that I worked on with Ashton Mining in the 1990s. The Merlin project is one of the best diamond projects not to have been developed. Merlin is a low hanging fruit in regards to the stage of a diamond project. What I like about Lithoquest is that they have discovered something different. If the indicator minerals are pointing to the source rock taping that elusive diamond stability field, then we are indeed looking at total different potential.

Remember, the potential of the diamond-bearing source rock is all about the ability to tap that region where diamonds are stable and are “formed”. The excitement is in the discovery of gem-quality diamonds from documented stream samples throughout the area, including a 1.73-carat diamond and three micro-diamonds found in a 10kg sample in 2018. The diagram above is highlighting the potential of what may be at play. Defining a pipe could be like trying to find the core of a porphyry system, finding the Low pyritic shell, the pyrite shell, the distal…etc. The defining of the pipe architecture is expensive but essential to uncover the motherlode of the pipe.

The other part of Lithoquest that I like is that I hear (not confirmed) that the Seppelt Diamond project is now within their project area. I don’t think this was part of the equation when I made my Coffee with Samso with Bruce Counts. I must remember to bring this up the next time I speak to him. Seppelt was last worked by Striker Resources (morphed into Myanmar Metals Limited, I think) in the early 2000s.

Here is an excerpt from an article from The Age in October 2002,

A 183-tonne bulk sample of Striker’s Seppelt 2 kimberlite pipe in the northern Kimberley yielded 412 carats of commercial-size diamonds. Striker said the indicated average grade of 2.25 carats per tonne was on face value, a world-class grade. Normally, grades at operating diamond mines are measured in carats per hundred tonnes. The exception is the Rio Tinto-owned Argyle mine, which grades 5-10 carats a tonne, albeit at a low average per carat value. Striker chairman and industry stalwart Ewen Tyler said the results were the best since the discovery of Argyle 25 years ago. “The most important aspect at this stage is the number of large diamonds in the sample, which is a very positive pointer for the value of what we are seeing at Seppelt,” he said. “Out of 412 carats from this 183-tonne sample, we have four diamonds greater than two carats, 21 greater than one carat and many greater than half a carat. The largest diamond to date weighed in just under three carats,” Mr Tyler said.

There is no doubt that Seppelt is diamond-bearing so if Lithoquest does have this, I think we are looking at something special.

The third diamond activity in Australia belongs to a private company called GeoCrystal Limited. The Webb Project which I wrote about The Webb Project: GeoCrystal Limited – The Next Diamond Story has a very interesting story. This will be the focus of the first Coffee with Samso for 2020. This should be published in the coming week.

Canadian listed companies that are exploring for diamonds.

(source: Bruce Counts CEO of Lithoquest Diamond Inc. (TSX-V: LDI))

Arctic Star Exploration (TSX-V: ADD) Head Office – Vancouver Shares Outstanding – 25.9m Recent Price – C$ 0.065 CEO – Patrick Power Website – https://www.arcticstar.ca/

Arctic Star has been exploring for diamonds for more than a decade. Currently, its flagship project is the Timantti Project in Finland where it has discovered several diamond-bearing kimberlite dykes and pipes(?). The company also has projects in the Lac de Gras region of the Northwest Territories near the Ekati and Diavik diamond mines are located as well as remote parts of the Nunavut Territory.

Key technical people include Buddy Doyle (Diavik Diamond Mine discovery) and Roy Spencer (Gribb Diamond Mine discovery)

North Arrow Minerals (TSX-V: NAR) Head Office – Vancouver, British Columbia Shares Outstanding – 110.7m Recent Price – C$ 0.045 CEO – Ken Armstrong Website – http://www.northarrowminerals.com/

North Arrow has been actively exploring for diamonds for several years and is arguably the most successful Canadian explorer over the last decade. The company has discovered two new diamond-bearing kimberlite fields, Pikoo in Saskatchewan and Mel in the Nunavut Territory. North Arrow’s current flagship project is Naujaat located in the Nunavut Territory. This project hosts several large diamond-bearing kimberlite pipes (originally discovered by BHP). The pipes have a low-value population of white diamonds; however, there is a population of orange-yellow diamonds that may change the economics. A large bulk sample is required to confirm the grade, value and size-frequency distribution of the coloured stones.

Key technical people include Ken Armstrong (Diavik discovery) and Eira Thomas (Diavik discovery and current CEO of Lucara)

Olivut Resources (TSX-V: OLV) Head Office – Edson, Alberta Shares Outstanding – 57.8m Recent Price – C$ 0.05 CEO – Leni Keough Website – https://olivut.ca/

Olivut has been an on-and-off diamond explorer for several years. The company’s flagship project is the HOAM project in the western Northwest Territories. HOAM hosts a number of weakly diamondiferous kimberlites. The company recently optioned and drilled a diamond project near Great Bear Lake in the NWT. Results of that drill program are pending.

Key technical people include Leni Keough (Diavik discovery), Dr Malcolm McCallum (Sloan discovery) and Martin St. Pierre (Ekati discovery)

Pangolin Diamonds (TSX-V: PAN) Head Office – Toronto, Ontario Shares Outstanding – 160.3m Recent Price – C$ 0.05 CEO – Dr Leon Daniels Website – https://pangolindiamonds.com/

Pangolin has seven early-stage projects, all of which are located in Botswana. The company’s flagship project is Malatswae where there is evidence of a kimberlite field in the form of KIM and diamonds recovered from loam samples.

Key technical people include Dr Leon Daniels (several discoveries in southern Africa)

Tsodilo Resources (TSX-V: TSD) Head Office: Shares Outstanding – 45.3m Recent Price – C$ 0.085 CEO – James Bruchs Website – http://www.tsodiloresources.com/s/Home.asp

Tsodilo’s key project is the BK-16 kimberlite in Botswana’s Orapa field. The kimberlite is relatively low grade but may have a population of large type IIA diamonds similar to Lucara’s Karowe mine in the same field.

Star Diamond Corporation (TSX: DIAM) Head Office – Saskatoon, Saskatchewan Shares Outstanding – 428.2m Recent Price – C$ 0.36 CEO – Ken MacNeill Website – http://www.stardiamondcorp.com/

Star Diamond has an advanced diamond project in north-central Saskatchewan. The Fort a la Corne kimberlite field hosts some of the largest kimberlites globally. The project has been active for more than two decades and is currently under option to Rio Tinto.

Key technical people include George Read (formerly with DeBeers)

Included in the list of explorers was a list of companies that were producing diamonds.

Canadian listed companies that are producing diamonds.

(source: Bruce Counts CEO of Lithoquest Diamond Inc. (TSX-V: LDI))

Lucara Diamond Corp (TSX: LUC) Head Office – Vancouver, British Columbia Shares Outstanding – 396.9m Recent Price – C$ 0.88 CEO – Eira Thomas Website – https://www.lucaradiamond.com/

Lucara has one asset: a 100% interest in the Karowe diamond mine located in the Orapa kimberlite field in Botswana. The deposit was purchased from De Beers and ownership was consolidated by Lucara. The south lobe of the Karowe kimberlite complex has a population of large, top-quality Type IIA diamonds that have made the company very profitable in past years and has produced some of the worlds largest diamonds. The company has recently completed a feasibility study to determine the economics of transitioning from an open pit to an underground mine. Lucara is believed to be scouting for possible acquisitions and/or mergers.

Lucara has also acquired a block-chain based marketing platform, Clara, that aims to align buyers of rough diamonds with specific stones. The platform is still in the ramp-up stage but aims to sell diamonds other than those produced at Karowe. It remains to be seen if this will be a profitable acquisition; however, it speaks to managements desire to broaden the revenue stream while staying within the diamond industry.

Mountain Province Diamonds Inc. (TSX: MPVD) Head Office – Toronto, Ontario Shares Outstanding – 210.1m Recent Price – C$ 1.14 CEO – Stuart Brown Website – http://www.mountainprovince.com/

Mountain Province has a minority interest (49%) in the Gahcho Kue diamond mine located in the Northwest Territories of Canada (De Beers owns the majority interest). The mine is known to produce lower-quality stones and stones that fluoresce. This has put a great deal of pressure on the profitability of the mine given that average price per carat of their production has declined by nearly 50% since the feasibility study was completed. Adding to that pressure for Mountain Province is the servicing of the debt incurred to fund their portion of the mine’s CAPEX.

Mountain Province has a 100% interest in the Kennady Lake kimberlites which is an advanced project and located very close to the Gahcho Kue diamond mine. While the Kennady kimberlites are small, they are high grade. It is speculated that the Kennady kimberlite will be acquired by the Gahcho Kue Joint Venture in the future when the current mine nears the end of its life.

Diamcor Mining Inc. (TSX: MPVD) Head Office – Kelowna, British Columbia Shares Outstanding – 65.3m Recent Price – C$ 0.095 CEO – Dean Taylor Website – http://www.diamcormining.com/

Diamcor has a single asset: a 100% interest in the Krone-Endora at Venetia Project. The project is focused on recovering diamonds from colluvium and alluvium down slope/stream from DeBeer’s Venetia diamond mine. Technically, the project is still at the bulk-sample stage since Diamcor has not produced a regulatorily compliant resource; however, effectively, the company is at the mining stage.

Australian listed companies that are exploring for diamonds.

Lucapa Diamond Company Limited (ASX: LOM) Head Office – Perth Shares Outstanding – 467.20m Recent Price – AUD$ 0.135 CEO – Stephen Wetherall Website – https://www.lucapa.com.au/

Commercial diamond production commenced at Lulo in 2015 through alluvial mining company Sociedade Mineira Do Lulo. The average US$ sales prices achieved for Lulo diamonds are among the highest of any alluvial mine in the world.

Kimberlite exploration is conducted by the Lulo partners through the separate Projecto Lulo joint venture. This exploration is designed to locate the hard-rock sources of the exceptional Lulo alluvial diamonds.

Lucapa is the operator of both the alluvial mining and kimberlite exploration activities at Lulo.

Gibb River Diamonds Limited (ASX: GIB) Head Office – Perth, Western Australia Recent Price – AUD$ 0.045 Executive Chairman – Jim Richards Website – http://www.gibbriverdiamonds.com.au/

Gibb River Diamonds is a renamed company from decades ago. I have lost track of how many. The last name was Poz Minerals, and I am not sure if it had Blina Diamonds. The main project is the recent acquisition of the Ellendale Diamond mine. Famous for its yellow diamonds, it was a great money generator for its previous owners until the major buyer decided to stop taking the stones. Since then, it has just gone downhill with the company going into administration and the tenements being tendered out.

The Blina Diamond project is of particular interest to me as it offers something different. If they can make this work, it will be something new and not dependent on the old Ellendale story.

Conclusion

Diamond geology/mining/exploration is my favourite topic, so this article has gone that extra length. As they say, you learn something every day, and I have learnt that the Canadians are way ahead in the diamond game compared to Australia. When the rush was happening in the 1990s, Australia was the go-to place. The discovery of Argyle and Ellendale prior was the catalyst for the rush in the 1970s to the 1990s. In the early 1990s, Stockdale (De Beers) had almost exited the scene while Ashton and Great Central Mines Limited were the leading players. There were other smaller players, but they never succeeded, such as Striker Resources and Moonstone Diamond Corp.

Most of the famous diamond mines have been operating for decades, and these mines are producing millions of carats per year. As I described earlier, Ekati and Diviak produced multiple of millions of carats per annum. Argyle Diamond Mine had a low gem-quality count, but it was the largest diamond producer in the world at one time. Argyle is famous for its pink diamonds. Argyle is also renowned for its marketing of simple brown diamonds as cognac and champagne diamonds.

It is evident that diamonds are found worldwide. The point of this article was really to highlight the complexity of diamond exploration and the risk/reward ratio, which is making fundraising difficult. What I did discover from this article was that there are a lot of explorers in Canada and numerous mid-tier producers. The Australian contingent is lagging. However, some surprises could turn the tide.

In Australia, I think Lithoquest and Gibb River could turn the momentum of diamond exploration if they make their projects work. For Lithoquest, confirming diamond-bearing kimberlites in their project area would create a new diamond region previously unknown. If Seppelt is indeed within the project are of Lithoquest could springboard the company into a possible near-term diamond producer.

For Gibb River, convincing the capital market that a rejuvenated Ellendale mine for yellow diamonds will make money will make them the most definite candidate to be the next diamond miner in Australia and indeed the world. Proving that the company can make money mining the yellow diamonds will put Gibb in an extraordinary place in the diamond mining club.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer or solicitation to subscribe for, purchase or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints. Read full Disclaimer.

www.samso.com.au

If you find this article informative and useful, please help me share the information. I try and write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters.

If you or your organisation see the benefit of what Samso is trying to achieve and have a need to share your journey, please contact me on noel.ong@samso.com.au.

Comments