4 Best Nickel Stocks - Awaiting a Happy Ending on the ASX

- Veronica Lind

- Sep 28, 2018

- 9 min read

Updated: Apr 10, 2022

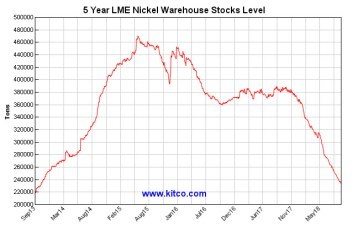

In 2016, I started telling people to be excited about Nickel stocks. First of all, they should start looking at the best Nickel stocks that are unloved now and awaiting a Happy Ending. The LME (London Metals Exchange) started to show a decreasing warehouse stock level. Also, the nickel price looked like it was bottoming out. Most noteworthy, it gave me the impression that the declining curve had taken a slight deviation. Consequently, the interest for Nickel is now a matter of history thanks to the Cobalt bull run. In addition, the word was out that the Li-Battery needed more nickel than cobalt …etc Oh yes, and suddenly every nickel projects became Ni-Co projects… 🙂

My Thoughts

However, my optimism is more related to the whole base metal market rather than just Nickel. In my opinion, we have just come off one of the worst commodity crises. So I felt with that prolonged downturn, it cleared out a lot of underperformance. This normally meant that productivity will slowly set in for the long run. Certainly a shallower but definitely longer wavelength of growth.

Industry people tell me that there is currently about 25 weeks of surplus on the LME. The stockpile, and according to the industry, needs to come down to within 10 weeks and that will start to move the price.

In regards to the supply issue, the general consensus from industry people is that the supply crunch will come in 2 years time. This is the kind of timeline that the current producers and near-producers are aiming for their projects to be at maturity. Companies such as Panoramic Resources Limited are now restarting their Savannah Underground Nickel Mine in the East Kimberley, Western Australia. So I am guessing that the journey has begun.

It is because of this factor that I like some of the lower ranks… The unloved or unknown stocks. So I came up with the 4 Best that I like. I was going to do 5, but I got lazy… 🙂

Panoramic Resources is a company that I tag as a Valued proposition. They are miners. There are the Western Metals, Mincor, Norlisk, BHP, Eramet…. etc. These companies are not what I think are the unloved/unknown stocks. I am not saying that they are of no good, in fact, I think they are very worth looking at as when things kick on, they are going to be money earners for everyone.

I just bought some Western Metals… hopefully, that is a good move :-).

Legend Mining has come on the scene with the Rockford project, located in the Fraser Range province of Western Australia. The project is a joint venture between Legend (70%) and Creasy Group (30%) with Legend being the operator. The concept is to find a Nova-Bollinger style nickel-copper and Tropicana gold mineralisation.

The project is has a large tenure. In fact, a total of 12 contiguous Exploration Licences covering 2,792km2. It is 120km northeast of the Nova-Bollinger nickel-copper deposit, owned by Independence Group NL.

As you can see in the diagram below, it lies along the strike of the large Gravity anomaly that house the Nova-Bollinger nickel-copper deposit.

Nickel exploration is not easy and finding that Ni-S body is a lot harder than your typical gold deposit. As a geologist who has limited nickel exploration, I have been told by good authority that finding a Ni-S body is very hard. However, with the new technological advances in geophysical tools, it is easier now than before. As I am told.

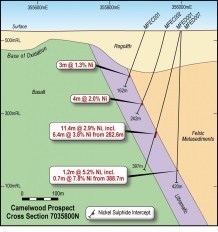

The diagram below illustrates why this is a good story. As you can see, there is good sized mineralisation grade complimenting a decent length of mineralisation. Always good to see some meterage in your intercepts. There is no doubt that this is a greenfield project but so was the Nova-Bollinger mine and DeGrussa. In fact, so was many other projects.

The exploration that has been done by Legend is proving that this is a relatively safe bet.

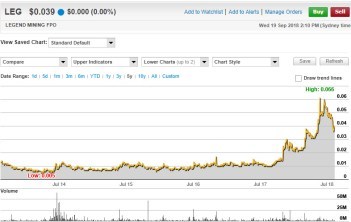

Price Chart

The price chart activity is certainly more active within the last 12 months. It’s obvious that the activities are clearly related to to the Rockford project. A joint venture into one of Mark Creasy’s projects seems to be the flavour of the month. Since cashing out from the Novo-Bollinger project (Sirus Resources LImited), Mr Creasy has had a few more wins so I will envisage that LEG will certainly be on many watch screens in the investing sector.

The only disadvantage I see is the Market Cap of AUD80M. It is pretty high for an explorer.

The most important concept to remember is that Mark Creasy has a 30% stake in the project and a 28% stake in Legend Mining Limited. This is a Mark Creasy company and if they get a sniff of success, there will be no issue finding new money to continue.

Rox Resources Limited (RXL) is a very interesting company.

AUD15M cash

EV of 3M

Market Cap of 15M.

East Fisher Nickel Project – Mineral Resource of 2Mt @2.5% Ni for 50,600 tonnes contained nickel.

Mt Fisher Gold Project – Mineral Resource of 973,000T @ 2.75 g/t for 86,000 oz contained gold. (To be divested into another new IPO in 2018/2019).

Collurabie Nickel Project – Inferred Resource of 573,000T @ 1.63% Ni, 1.19% Cu, 0.082% Co, 0.85 g/t Pt, 1.49% g/t Palladium.

The East Fisher project was discovered in 2012. In fact, I reviewed the project and wanted to put in a bid to buy it for my previous life. Originally, this is a gold project and I felt that there were limits to the project. I still think that is the case. The location is pretty remote and you would need to find a lot more to make the gold work. What I did not expect was the discovery of the nickel in the project. This I feel will make a difference. The discovery of the nickel is a game changer for RXL and I hope they can make this work. In addition, with the addition of Collurabie Nickel Project, this company could provide a few surprises.

I am surprised that with the discovery, things have not really happened for RXL in the share price department. I was a shareholder a few years ago and sold out making some coin but it seemd to have stayed pretty much stagnant since that time.

The photos above are some samples from East Fisher. I spoke to Ian Mulholland about the prospectivity and he explained that the ore bodies are still open and there many upsides to the story. The good part of these deposits is that they are shallow and within 70km from the nearest mill. Collurabie is further east but when you look at the final picture, I think this is a workable project. There are definitely some negatives, but they have the money to do the work required.

The mineralisation from a geologist point of view is interesting. For me, at this stage, I am enjoying the whole geological story. I wished I was this studious when I was doing the geological degree.

Price Chart

If the nickel price does head north, this will give RXL a lot of room to move. However, the 5-year chart below shows that there is a disparity between what the potential of the company and what the market values it. This is one of those issues when a company has legacy issues and the market just does not like you. Looking at the stock, there are about 1.3B shares and that does scare some real investors away. The stock has traded in a downward trend for too many years for a company with AUD15M in the bank. Just does not make sense.

I think they need some chinamen in there to stir the pot… 🙂 Only a chinaman can make leftovers a staple dish… Fried Rice… Long soup…Short soup…

Talisman Mining Limited (TLM) is another company that I feel is worth a good read. They had the tenement adjacent to Sansdfire Resources Limited and when they announced the discovery of the DeGrussa deposit, and TLM share price went flying. The management comes from good history, ex Jubilee Mines NL. If I am correct, Jubilee Mines sparked off the last run of nickel discovery in the early 2000s. The industry was having a hangover from the 1999 disaster, and the discovery of nickel was sparking the workflow.

After the discovery of DeGrussa, TLM worked on their Springfield project (the one adjacent to DeGrussa) and discovered the Monty Copper Mine. As I write, they have recently announced that they have sold that project for $AUD70M + to Sandfire with extras. So for a small company, that is a good result. As you can see in the price chart below, it is not a bad investment/punt for the investor.

The discovery of Monty would make a good read too. Maybe I will see if I can do something about that in the future.

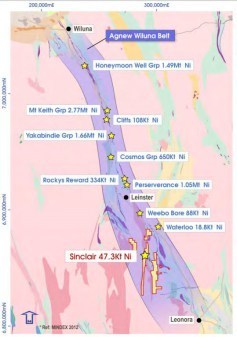

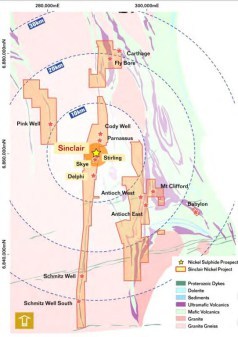

The Sinclair Nickel Project

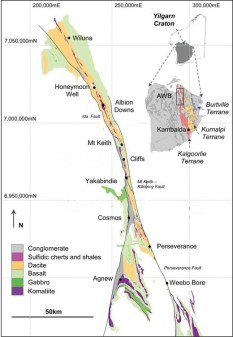

This is located in the famous Agnew-Wiluna Greenstone belt. Probably the best known world-class district for Ni mineralisation. It is a historic mine. It has produced 1.58Mt @2.44% nickel for 38,599t of nickel from 2008 to 2013. The site has all the infrastructure for a working mine and has been under care and maintenance since the downturn of the nickel price. I am no expert in Nickel but my understanding is that as these lodes are very small but have high grades, so the chances of finding more are very high. Look at the Kambalda nickel mines. They have been producing for decades.

Assuming that the management is not planning to mine the market and are really making an effort to make this work, I would bet money on finding more workable lodes of nickel sulphides. What I do know about nickel sulphides is that they are damn hard to find. As a result, when you do find them, they tend to be something that can work. Consequently, from an exploration point of view, I would say that I will rather be exploring at a place where there is much smoke and have been known to be flammable. Furthermore, always remember that they are in a well know nickel province.

I know I sound like I am repeating myself, the reason I like Talisman very much now is that they are going to have a heap of cash and they have good ground to drill. To top it all off, there is a great chance that the nickel price will go up. Looks like a good combination to me.

From the last published presentation, I like the look of their interpretation, strike extension and the grades look very consistent.

Poseidon Nickel is something of an oddball. I actually know very little but the latest corporate moves make me think that I am missing something. I know what they have technically. How anyone would want to pump lots of money into the company makes me think that there is something that I have not understood. Most importantly, I know that they a very high-grade Nickel mine, Silver Swan which is within the Black Swan Project.

Price Chart

Looking at the price chart, there is nothing there that will excite most people. For instance, the lack of spikes and I mean noticeable spikes is boring. However, I do know that there are a lot of big wigs in this stock. So if there are corporate moves, one must take note and start asking questions. The latest manoeuvring corporately makes me more than interested.

Black Swan

The project is 600km east of Perth and 50km northeast of Kalgoorlie, Western Australia. There are three components to the project,

Black Swan open pit

Silver Swan underground mine.

Black Swan sulphide concentrator (2.15Mtpa) and supporting infrastructure.

The Black Swan deposit contains serpentine ore (0.74% Ni) and talc carbonate ore (0.72%). The Silver Swan underground mine contains 147,000T @ 11.48% Ni for 17,000T contained Ni

What’s Happening with the Project

First of all, as I have mentioned, there was a flurry of activities the last few months culminating in the latest scenario. There had been many talks in the street that something was happening and as a result, I have sort of kept abreast on the goings of POS. Not diligently but it was in mind. The result was the resulting capital raising that made headlines. The latest fundraising is apparently going into the restart of Silver Swan and Black Swan. There are also talks about exploration drilling in several of their prospects. The good news is that I am bullish on the nickel price. Companies like POS will be in the box seat with a rising Nickel price. They have the infrastructure and the mines. Their pricing is unloved and this is why they are on my list of things to watch.

They have a Market Cap of AUD100M and I guess for a miner, that is not too high. Share price sucks but if they can make Silver Swan work again, then things may change.

Finally, I recently saw an article by SmallCaps, regarding the exploration of the Abi Rose high-grade nickel discovery that made a good read.

Disclaimer

The information or opinions provided herein do not constitute investment advice, an offer or solicitation to subscribe for, purchase or sell the investment product(s) mentioned herein. It does not take into consideration, nor have any regard to your specific investment objectives, financial situation, risk profile, tax position and particular, or unique needs and constraints. Read full Disclaimer.

www.samso.com.au

If you find this article informative and useful, please help me share the information. I try and write about topics that are interesting and have the potential to be of investment value. It is not easy to find stories that fit those parameters.

If you or your organisation see the benefit of what Samso is trying to achieve and have a need to share your journey, please contact me on noel.ong@samso.com.au.

Comments